It´s pretty Well Impossible to Have a Passive Dividend Income Strategy

You Have to Actively Manage an Investment Trust Income Portfolio

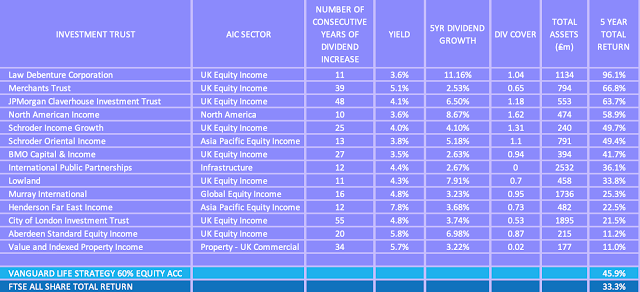

The AIC Investment Trust Dividend Heroes

Selection Criteria

-

-

-

-

-

- 5 Year Dividend Growth

- Dividend Cover (years)

- Total Assets

- 5-year Total Return

-

-

-

-

- Minimum Yield 3.5% - roughly the safe withdrawal rate (SWR) of a drawdown portfolio

- 5 Year Dividend Growth Rate >2.5% - should at least beat inflation

- Assets > £100m. Small Investment Trusts are vulnerable to mergers and closures and will not attract the best managers.

Two benchmarks are shown, the Vanguard 60% Equity LifeStrategy fund and the FTSE All-Share total return. The graph below compares the 5-year performance (total return) of a portfolio of 9 Income Investment Trusts with the two benchmarks.

Conclusions

I will be looking in more detail at some of the shortlist ITs in my next post when I will be examining the performance of my Investment Trust Retirement Income portfolio.

Today it is certainly more difficult than 5 years ago to put together a diversified portfolio of Income Investment Trusts that fulfill my main criteria. Several of my original portfolio constituents that met a key criterium of dividends surviving the 2008 crash have now fallen by the wayside and only 9 ITs in the list have an increasing dividend history post-2008. This again highlights the need for portfolio monitoring.

My final shortlist is shown below:-

(It should be noted that infrastructure companies are like REITS and don´t have significant revenue reserves.)

It’s quite possible that we haven´t had all the bad news about possible dividend cuts from all the Income Investment Trusts so if the intentions of a particular company aren´t clear it would be wise to wait at least 12 months before investing.

It would be wise to have more geographical diversity in a portfolio by including a European Trust but there are few candidates that get close to the selection criteria. The best of the bunch is JPMorgan´s European Income that offers an acceptable yield and has had over 5% annual dividend growth over the last 10 years (but has had several years of static payouts.)

Looking to the future, the dividend cover of many companies has fallen post-Covid and this must raise a warning flag. From 2009 to 2019 we have had 10 years of rising markets and increasing dividends which have allowed Investment Trusts to strengthen their reserves. If the next decade is characterized by weak market performance many of the companies will be unable to rebuild their reserves and this will put dividends at risk when the next crisis hits. This emphasizes the need to select companies with good dividend coverage and companies that have shown commitment to maintaining or increasing dividends post the Covid dividend crisis.

.