The idea of living off the natural yield of your investments and not touching the capital is widely criticised as a strategy in most financial publications and blogs. However, the attractions of a dividend income strategy for a retiree are clear:-

- No worries about running out of capital

- No worries about choosing an initial withdrawal rate

- No worries about a market collapse in the early years of drawdown

- The potential for a higher initial income of 4%+ compared with a “play safe” 3 to 3.5% initial withdrawal rate for drawdown

- The possibility of leaving a substantial inheritance

- Dividends are just a return of your own money - a 5p dividend on a 100p share leaves you with a share worth 95p and a likely tax liability.

- Shares which have high dividend yields are low growth

- Reduced diversification. A portfolio based upon above-average yields will by definition eliminate 50% of possible companies in particular those which provide high growth.

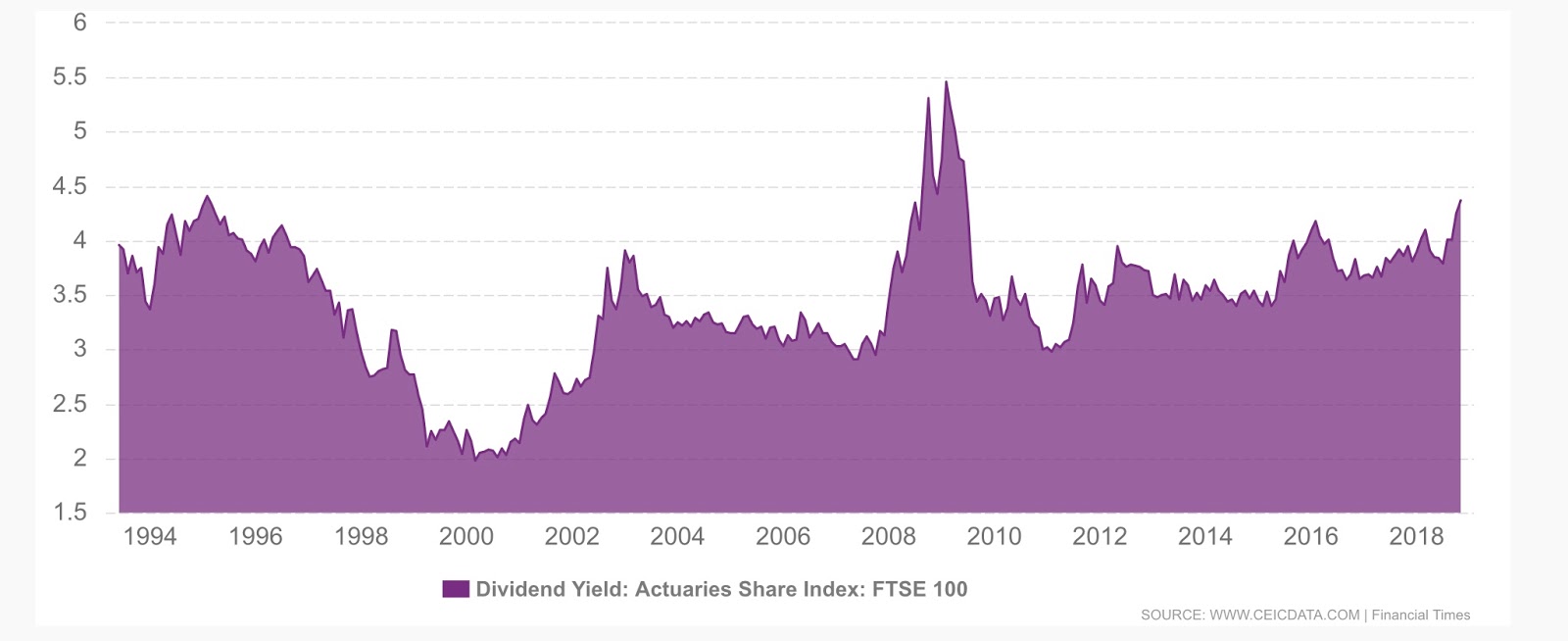

- Limited International Diversification. The USA represents 43% of the global market but the S&P 500 only yields 1.8% compared with 4.35% for the FTSE100 and 4.06% for the FTSE All Share which can lead to an over-concentration in the UK market which only represents 5% of the global market and had a return over the last 25 years of 6.4% compared with 10.1% from the S&P500 (dividends reinvested).

- Dividend income is lower than can be obtained through a withdrawal strategy

- Companies can cut dividends during difficult economic times

- Possible adverse tax implications if the portfolio is outside a tax-exempt wrapper

(ii) A high yield on a share often signifies a downrating of the share by the market, possible reduced profits and maybe a dividend cut. There are also shares that due to their market sector -utilities, tobacco, oil etc. distribute a higher percentage of their profits in the form of dividends and are likely to be lower growth but maybe a less risky investment. In a report by JP Morgan “US Dividends for The Long Term” it is actually shown that dividend-paying large-cap shares outperform non-dividend payers and that demographic changes will favour dividend payers.

(iii) Certainly lack of diversification both within particular markets and internationally is a concern and sectors such as “small-cap value” which are highly recommended by respected advisors such as Paul Merriman and tech which has performed spectacularly over the last 5 years would be precluded from a dividend portfolio.

|

| 5 Year Performance: NASDAq +94%, S&P +58%, FTSE 100 + 8.75% (without dividend reinvestment) |

(iv) It is especially true of markets such as the USA that dividend yields are lower than can be obtained through a withdrawal strategy. UK yields are currently at a historic high (FTSE 100 over 4.3%), so it is easy for a portfolio to yield 4%+, however, the average FTSE100 yield over the last 25 years is nearer to 3% than 4%.

(v) Yes companies go bust, and companies cut dividends. One only has to think about regular dividend payers such as royal Bank of Scotland, Carillion, BP and Centrica, however, regular dividend payers cut the dividend as a last resort and prioritise its payment often cutting internal investment (not always a wise decision) or increasing borrowings in order to maintain the dividend - as often the consequence of cutting it will result in the CEO having to resign. A well-diversified income portfolio mitigates the effects of such cuts.

Other Considerations

The Price to Pay For Retiring on Dividends

My Strategy