We all all used to investment advisers reminding us that the stock market is a long-term investment and should only be considered for a 5 year plus investment. However, the publication of the Barclays Equity Gilt Study 2009 with its “lost decade” references resulted in much reappraisal of this with some commentators talking of 0-20 years as being a safer investment time horizon.

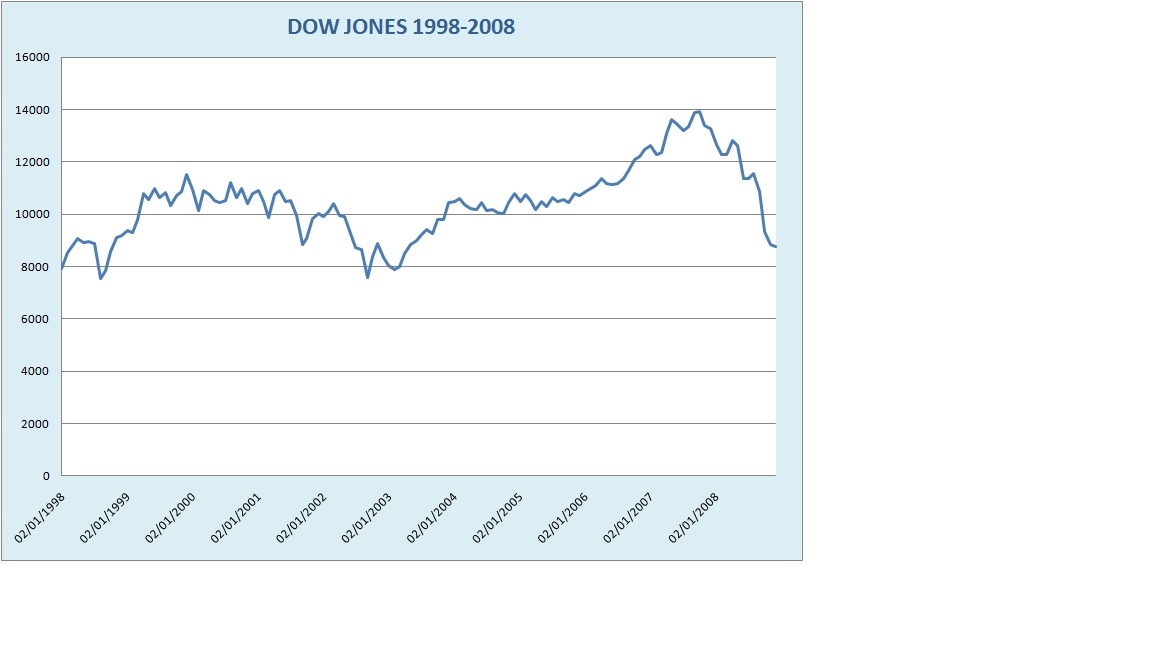

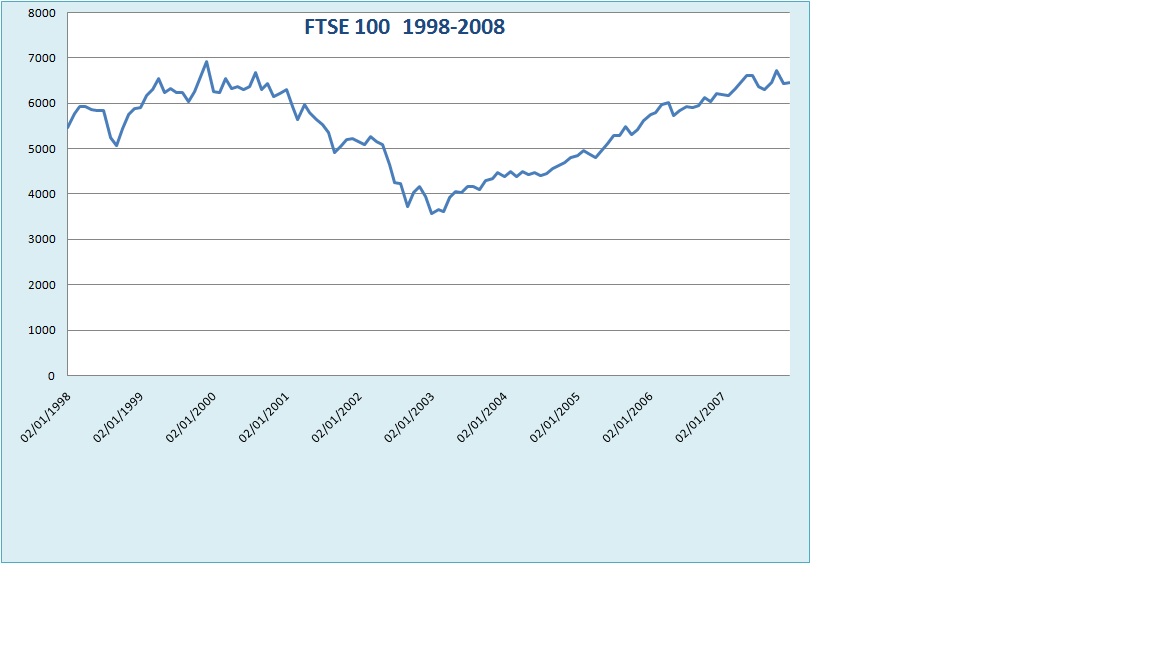

There appears to be something very illogical in the idea that if one invests in a portfolio of sound profitable businesses that it is impossible for a shareholder to share in their success. But this in fact is what happened in the decade following 1998 with a -0.3% annualised return from US equities and 1.05% nominal return from UK equities. Were McDonald’s, P & G, Johnson & Johnson, Glaxo, BP, etc. really doing so badly? Maybe not. But if you had invested in the Dow on the 2nd January 1998 your investment would have increased by a mere 2.7% over the next 10 years - without taking into consideration the dealing costs and the bid/offer spread.

The last consecutive decade in which stocks produced a lower real return than Treasuries, was 1967-77 in the US and 1927-37 in the UK. Barclays says during the past 110 years, there have been some 16, 10-year periods that bear resemblance to the decade just past and like in the past decade in which investors who prudently re-invested their dividends lost money after inflation - each time, they made money in the next ten years, by an average of almost 11% a year even after factoring in rising prices.

This unfortunately is Ben Graham’s “Mr. Market” coming into play. He is famously quoted as describing the market as a voting machine in the short term and as a weighing machine in the long term. Sometimes the “short term” can last a decade or more and the poor investor has to suffer the irrationality of “Mr. Market”. His only salvation are the dividends - and this is the reason I will never invest in a company that doesn’t provide a reasonable level of dividends and a demonstrable will to maintain the dividend during hard times and to grow it in line with profits during the good times. Remember that a company has only two ways to reward its shareholders - through share value growth and through dividend payments. Yes, a company can use share buybacks to try and bolster the share price but the shareholder reward is still in the hands of “Mr Market”. A dividend payout is out of reach of the psychotic “Mr. Market”.