My Final Retirement Income Plan (maybe!)

After 18 months or so of research, I`ve finalised my retirement income plan. £40k of net annual income weighted towards the first decade or so of retirement.

The income is derived from sources that are unrelated to stock market performance:-

-

-

-

-

-

-

-

- UK State pension

- Lifetime Annuity

- Side Hustle

-

-

-

-

-

-

and two that are stock market linked:-

-

-

-

-

-

-

- An Investment Trust Income Portfolio yielding 5%

- A Drawdown Portfolio using Variable Drawdown with an initial drawdown rate of 5.1%

-

-

-

-

-

I have sacrificed inflation-linked income for a higher initial income. In fact, it isn`t much of a sacrifice as even if inflation averages 4% long-term it is only after 23 years that an inflation-linked income would exceed the income from my front-loaded plan. In fact even if inflation was 9% over 25 years the total income received would still be greater with my plan.

Around 50% of the income is directly linked to stock market performance and given that the Investment Trust Income is likely to be maintained during a stock market crash then the income from the plan should be relatively stable.

Around £480K is invested in the annuity purchase and investment portfolios. A further £250K is dedicated to long-term investment to leave as a legacy or to deploy as an emergency backup. There is a £30k cash reserve for use in the event of a reduction in drawdown or dividend income. The tax burden is low as having been overseas for many years meant I was unable to benefit from tax relief on pension contributions. This made saving more difficult but now gives me the advantage of having investments outside of a SIPP which are taxed more favorably than pension income.

A Long Road to Devising the Plan

My research has involved exploring and writing about:-

-

-

-

- Buy-to-Let Property Investment

- Dividend Income versus Total Return

- The Role of Annuities

- William Bengen`s 4% Rule

- Portfolio Simulation Tools

- Portfolios for Drawdown

- Investment Trust Income Portfolios

- The Role of Gold In A Portfolio

- Variable Drawdown Strategies

- Income Harvesting (alternatives to periodic rebalancing)

- The Cash Reserve

- Planning for Cognitive Decline

-

-

There is No One Fits All Retirement Finance Solution

Retirement planning has attracted an enormous amount of academic interest and books, articles and websites abound. It is a complex area. There is no easy off-the-peg solution to the need of the retiree who doesn`t have a guaranteed retirement income through an inflation-linked pension scheme. Not only does the retiree has to plan for the extremes (high and low) of market returns and inflation rates but these have to be incorporated within a plan that is personalised taking into account factors such as:-

-

-

-

- Health and longevity

- Dependents

- The desire to leave an inheritance

- The flexibility of spending needs - can spending be easily reduced if necessary?

- Any future likely sources of income - perhaps an inheritance.

- The availability of state support for long-term care.

- The option of house down-sizing or equity release.

- Other available forms of income - side hustle, working part-time.

- The likely future spending profile - early years of high spending followed by a gradual decline, or U-shaped due to long-term health and care costs.

-

-

In my blog, I have tried to address some of the key issues which I hope will be helpful to many people planning their retirement income. Although retirement finance is for many the most important issue when planning retirement the ideal is for this to fade into the background so that the focus can be on having a few decades of enjoyable and fulfilling life. Research shows that purpose and family and social relationships are the two of the most important factors in contributing to a rewarding retirement NOT income.

Maximum Income is No Longer My Main Objective

I had initially set the objective of my plan as being to produce the maximum sustainable income with a higher income level during the first decade or so of retirement when hopefully good health would result in higher spending as long-held ambitions to travel Europe and the USA in a camper van and visit South America and Australia could finally be fulfilled. Of course not only did Covid intervene but health issues for my wife curtailed these plans as certainly in the medium term she cannot obtain travel health insurance.

So my revised plan allocated around two-thirds of my funds to providing income and the remainder is in reserve to provide an inheritance should markets perform well, or as a back-up should markets severely underperform or if I have the good fortune to live too long! My wife who, health-permitting, plans to continue working for the next 3 years has a good salary, will receive an inflation-linked pension, and has property assets so I have not had to include her in my planning.

Minimise Tax

Having spent a fair number of years overseas I have only been able to shelter some of my savings in ISAs and much of my retirement savings have been outside of a SIPP. The latter is a mixed blessing as although these funds haven`t benefitted from tax relief so took longer to accumulate at least income derived from these investments is potentially more beneficially taxed due to the use of the annual CGT allowance and lower dividend taxation. Not needing the maximum income has also allowed me to keep taxable income from the state pension, annuities, and the SIPP to around the annual tax allowance with this income supplemented by tax-free ISA income, rent-a-room income, and non-tax sheltered drawdown.

Some Pre-Retirement Actions

Sold My Buy to Let Properties. I`ve always believed that leveraged purchase of property can be a rewarding way to build up capital and I looked at this in some depth in my post The Stock market or UK Housing. The big investment advantage that property has is the ability to leverage the purchase and providing property increases in value the gains will usually far exceed that that could be obtained by investing the 20% or so deposit in the stock market. It is far from passive investment however and suffers many tax disadvantages. So wanting a hassle-free retirement I sold my two properties and invested in the stock market. I will progressively transfer these investments to ISAs.

Invested in Solar Energy. I estimated that an investment in solar PV and water heating would reduce my long-term outgoings and in effect give me a tax-free return on my investment of at least 10%. With the current energy crisis, it has proved to be a very sound decision.

House Extension. An investment to provide some relatively private accommodation in the house has provided a Side Hustle generating around £7000 pa tax-free under the Rent a Room Scheme.

Plan Summary

Income Sources (annual):-

-

-

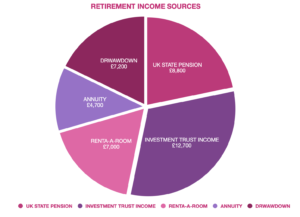

- UK State Pension £8800

- Lifetime Annuities £4700 (Cost £85,000)

- Investment Trust Income Portfolio (ISA) £12,700. (Portfolio Value £253,000)

- Drawdown Portfolio £7200. (Portfolio Value £140,000)

- Side Hustle Rent-a-Room £7000

-

Total Income £40,400

Tax (income and dividend) £400

Net Income £40,000

UK State Pension - fortunately, I had the good sense to pay Class 3 voluntary contributions during my spells overseas although due to changes in the rules I didn`t manage to obtain the maximum new state pension. It was certainly good value for money back in those days.

Lifetime Annuity - Partial Annuitisation allows a retiree to obtain a higher level of initial income than is possible through drawdown. Although the annuity income declines in real terms with inflation this also follows the spending pattern of many retirees who would prefer to have a higher initial retirement income to be enjoyed during the years of good health. Combined with inflation-linked sources of income such as the State Pension, Investment Trusts and potentially the Drawdown Portfolio the early years of retirement benefit from a higher income level, and with a higher proportion of income provided from guaranteed sources there is greater protection against the sequence of return risk.

I used £85,000 from my SIPP to purchase a level annuity paying £4700/annum. This is a 5.5% yield nearly 50% more than inflation-linked income drawdown would provide. I would have invested a higher amount but I wanted to keep my taxable income to around the annual personal tax allowance. My preference would have been a Purchased Annuity rather than a Pension Annuity so I could preserve investments within the SIPP to minimise inheritance tax but there are few providers and rates are significantly lower than from Pension Annuities although the tax treatment of Purchased Annuities is more favourable.

Investment Trust Income Portfolio. Retiring on dividends is a much-criticized strategy and certainly is not appropriate for a retiree who needs every penny of income and is not interested in leaving behind a legacy for his heirs . I have covered the topic in various posts (Living Off Dividends a Crazy Idea), and there are certainly many valid objections raised to the concept. Much of the negative sentiment comes from the USA where dividend yields are low and diividend tax treatment is unfavorable. Even a dividend ETF such as the Dividend Aristocrats only yields 2.2% so a US retiree would have a difficult time replicating the 3% to 4% income available in drawdown. However, there is much evidence that companies that are committed to dividends and have paid them without fail for decades outperform all other companies, and whilst managers have a hard time beating the indices it is a far easier prospect to construct a portfolio of companies that have a pretty good chance of paying increasing dividends over the long term. The UK investor has the advantage that UK companies have historically had a greater commitment to dividends with the FTSE 100 yielding over 4%.

The criticism of a dividend strategy that the income can vary is perfectly valid. Of course in practice, drawdown income is also likely to vary - if there is a 60% market crash there can`t be many retirees who would just sail blindly on taking an ever-increasing income, most are likely to cut back on their drawdown income until markets recover. The advantage of dividends is that it is very rare that they will fall as drastically as share prices but we only have to look at dividend cuts in 2020 to see that dividends are not guaranteed. Most Income Funds cut back their payouts severely. The exception was the Investment Trusts Income sector. Almost all maintained payouts resorting to their reserves if necessary (they are able to keep back up to 15% of their income in reserve). Of course, this is no different from a retiree keeping a cash reserve to see him through difficult market conditions but it is comfortable to have someone doing this for you.

I have invested in Investment Trusts (Investment Trust Income Portfolio) for over two decades in preference to funds that many years ago were expensive with 5% to 6% bid/offer spreads and 1% to 2% annual charges. Funds are now far more competitively priced but don`t have the transparency of Investment Trusts and for income- seekers lack the ability to smooth out dividend payments. As I do not need to maximise income at the expense of legacy then a portfolio of ITs offers me automatic regular dividend payments and no concerns about market ups and downs. The big drawback is that they are actively managed investments and managers and investment philosophies change so periodic portfolio reviews are essential. This is not ideal long-term when the likelihood of a decline in cognitive capability combined with poor decision-making is very possible. So I anticipate that in a decade or so I will have to swap to a total return drawdown strategy. In the meantime, I have around one-third of my investments in the IT Income portfolio below:-

I describe my methodology for choosing trust in my post Top Investment Income Trusts Choices. I am looking for trusts that:-

-

-

- Pay a dividend yield at least as high as a typical drawdown Safe Withdrawal Rate (SWR)

- Have demonstrated a strong commitment to increasing or at the very least maintaining dividends

- Have beaten the FTSE All Share Total Return over 5 to 10 years

- Pay dividends predominately from revenue, not capital

- Ideally, they should have the equivalent of at least one year of dividends in revenue reserves

-

One year plus of dividend cover is currently a rarity as whilst strong market returns had allowed most trusts to build up their reserves post 2018 crash, most had to dip into their reserves in 2020 in order to maintain their dividend payouts when a high proportion of UK companies were forced to cancel their dividends. For instance, City of London`s reserves have fallen to around 5 months’ cover.

The portfolio currently has a value of £253K, a yield of 5.1%, and pays out around £12,600 annually (free of tax as it is in an ISA). Dividend growth since 2012 has been 4.1% per annum compared to the RPI of 2.6%. However the future for dividend growth doesn`t look too rosy with poor market performance, high inflation and low revenue reserves probably the best case outlook is for the portfolio to maintain the current level of payout in the medium term. But 5% is a pretty good yield and hopefully, dividend growth will resume in a few years’ time.

Drawdown Portfolio. This is a £140k investment in a Vanguard General Investment Account split 70% FTSE All Cap and 30% Global Aggregate Bond. Vanguard certainly isn`t the cheapest platform once you have a reasonably sized portfolio with annual charges of 0.15%. IWeb for instance has no annual charge. However, the big advantage of Vanguard in drawdown is that you can specify a monthly, quarterly, or annual withdrawal amount and they will sell the necessary units in the proportion between funds that you specify. Other brokers require you to liquidate part of your portfolio periodically to provide the cash for drawdown - if you forget to do it - no payment.

Drawdown Strategy. Rather than use the classic Bengen x% initial drawdown with annual inflation adjustments I will be using my Variable Drawdown Strategy, This is an easily implemented strategy that permits a higher initial drawdown rate with future increases dependent upon the portfolio performance. The two big pluses of this strategy are the higher initial income and the option of taking more income or leaving a larger legacy - subject to market performance.

The strategy is very easy to understand and implement:-

-

-

-

-

- Decide upon an initial withdrawal rate - up to 1.5X a typical SWR is reasonable

- At every annual anniversary:-

- If the actual portfolio value is greater than the initial portfolio value then increase the income withdrawal by the rate of inflation. If not greater withdraw the same amount as the previous year.

- If the actual portfolio value is 1.5 times the initial portfolio then take a bonus of 5% of the difference between the actual and initial portfolio value or if you want to maximise the legacy just take the inflation increase.

-

-

-

I have adopted an initial withdrawal rate of £7,200/year paid monthly which is 5.1% of the initial portfolio value. In the worst case, the drawdown amount stays fixed for the entire retirement. With no increase in drawdown income Timeline predicts a 99% chance of portfolio success to age 95 with a legacy of £173k. If the portfolio performs well the drawdown amount will ratchet upwards. The 5% bonus payment is optional so if my finances are healthy I won`t take it in order to leave a larger legacy.

The Side Hustle. Extending the house to provide extra, fairly private, accommodation had two motivations. Firstly to provide some additional income without losing too much privacy but the other motivation was looking long-term in case either my wife or me or both need a live-in carer. Welcoming guests into the house has been generally a very agreeable experience and the income means I leave some investments untouched, hopefully, to grow. These investments can be used to replace the side hustle income at some future date.

£40,000 Net Income, £400 tax.

The chart below shows the distribution of the income. Total investment in the annuity, Investment Trust Portfolio and Drawdown Portfolio amounted to £480,000. The annuity payment is fixed and the income drawdown is assumed to be fixed although if market performance is good it will rise. The other income sources which represent around 70% of the total annual income are assumed to be inflation-linked.

Stock market Vulnerability. 50% of the portfolio is linked to stock market performance (Drawdown and Investment Trust Income). Income from the Investment Trust Portfolio is far less volatile than the stock market but they are not immune to having to reduce payouts by probably 25% or so in the worst case (around £3000). Although historically the Drawdown portfolio should survive a severe market downturn, it would be reasonable to expect that I would reduce the level of drawdown until markets recover, say a cut by 50% (£3600). So in a worst-case situation, I could experience a reduction of £6600 in annual income (-16.5%).

Cash Reserve. There are two reasons to have a cash reserve:-

-

-

- To smooth out cash flow both income and expenditure and to have ready cash to cover those sudden expenses such as car and house repairs.

- As a funding source during market downturns to avoid selling stocks at deflated prices.

-

In the first case, I just keep a reasonable amount in my current accounts to cover these situations and to smooth out the dividend payments for the Investment Trust Portfolio. Until the recent market downturn in both equities and bonds, I was happy with the idea of just drawing down on bonds rather than equities if equities crashed. The recent fall in bond prices shows that this is not a guaranteed winner! So I have created a short-term cash fund of around £30,000 to provide 5 years or so of income top-up.

Inflation Effect on Income. The object of the plan was to bias the income towards the earlier part of retirement anticipating a decline in spending towards the latter years. Achieving this by combining higher payout non-inflation-linked income sources with inflation-linked sources. The largest later-life expense is likely to be long-term care which I expect will use my house as the main source of funds. It really isn`t practicable to provide for what could be a few months of residential care or a decade or more of care.

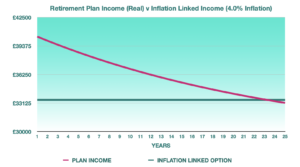

The graph below shows the projected income in real terms assuming an annualised 4% inflation rate compared to the income that would have been received if all the investments had been placed in a drawdown fund with annual inflation-linked income increases using an initial 3.75% withdrawal rate. A fully inflation-linked plan would have produced an initial income of £33,725 compared to £40,000. The income from my front-loaded plan decreases every year by the rate of inflation but it is only in year 23 that the inflation-linked income exceeds the plan income.

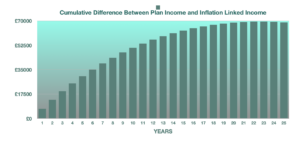

The graph below shows the cumulative benefit of this plan against taking an inflation-linked income. Over 25 years you are over £70,000 better off with this early-years weighted approach. If fact you would have to have inflation of over 9% per annum to be worse off over 25 years by choosing the front-weighted plan.

The Back-Up

Around two-thirds of my investable assets have been allocated to this plan. The remainder is divided into two “pots”:-

-

-

- Long-term back-up or Inheritance SIPP. Hopefully never to be touched (by me) but available as an additional income source through annuity purchase or drawdown 15 to 20 years in the future. My ideal would have been a Target Date fund to glide path from 80% equity to 30% over 20 years. Unfortunately AJ Bell my SIPP provider charge 0.25% annually for fund holdings. This would result in annual fees of £300 rising to over £600 over a 10-year period compared to around £140 for an ETF portfolio. So I am going with ETFs and will implement my own glide path increasing the bond content by 1.5% to 2% per annum.

- Medium-term General Account back-up. This will provide an income substitute through drawdown for the Rent-a-Room income when I finally end this side hustle and will gradually switch from General Account to ISA.

-

The Plan is on Auto-pilot

My retirement income plan requires less than one day per year for maintenance:-

-

-

- Re-balance the drawdown portfolio and check whether the monthly drawdown amount can be increased.

- Re-run the Investment Trust Income analysis and check the new top performers with the existing portfolio constituents. Eliminate and replace if necessary.

- Transfer assets to ISA

-

The four main income sources are paid automatically and in fact, if there was no annual review the payments would continue pretty well for many years if not forever:-

-

-

- UK State pension

- Lifetime Annuity

- Investment Trust Income Portfolio

- Drawdown Portfolio

-

Long Term Financial Management

It would be fanciful to think that as I age that I will maintain my mental abilities in the same way as Warren Buffett and Charlie Munger have. It is more probable that I will suffer some degree of cognitive decline. As I highlighted in my post How to Protect Your Retirement Finances From Cognitive Decline one of the greatest dangers is not the severe and easily recognisable mental impairment associated with Dementia of Alzheimers but the gradual deterioration in decision-making capability combined with an over-confidence in one`s decisions. I may be sufficiently competent to manage my finances during the next decade or so but there is no guarantee that I will be mentally capable forever.

I am not so fortunate in having close family who would be able to identify any mental deterioration and take over the running of my finances. Without a doubt, I will need to make decisions about my investments before the onset of cognitive decline. Over the next 20 to 30 years there will be changes in the investment environment perhaps a greater emphasis on asset classes other than equities and bonds. Maybe Crypto will truly become an asset class rather than for speculation. Perhaps there will be innovations in retirement income products to supplant the lifetime annuity. This means that it is inevitable that investment choices will need to be made and it is probable that a retiree in his 80s isn’t going to be the best person to take such decisions.

Over the next decade, I will be trying to simplify my investments in order to minimse the decision-making that is required. Unless I am exceptionally fortunate in maintaining my mental faculties (or unfortunate if I die early!) then it is inevitable that I will have to hand over my financial management to an advisor. Although paying 1% to 2% annually is very unappealing but so is the thought of making a catastrophic mistake and ending up in poverty. Hopefully, I have time on my side to make a decision and it certainly would be welcoming to see Vanguard extend their low-cost advisory service to include post-retirement advice as they do in the USA.

Things I`ve Learnt

Accumulation is far easier than deaccumulation. Judging by the wealth of books, and articles dedicated to retirement saving one would think that the accumulation phase is extremely complicated. It isn`t. The majority of savers can contribute to a low-cost global fund for all but the last 10 years prior to retirement and then progressively de-risk their portfolios by adding bonds. Even simpler is the use of a Target Date Fund with the saver only having to choose a target retirement date that will give him his preferred equity/bond ratio on entering retirement. If the pre-retiree is missing his “pot” target he has the option of upping his savings or delaying retirement.

However, the retiree has to contend with three key variables:-

-

-

- Stock market performance

- Inflation

- His and his partner`s longevity

-

Only the lucky few with an inflation-linked pension, or with sufficient funds to purchase an inflation-linked annuity will be 100% guaranteed to be able to cope with all possible outcomes of these variables. The majority of retirees have to devise plans that statistically should cope with historical market conditions and inflation and projected longevity

Simplicity is a virtue. There are well-publicized portfolios with 10 or more constituents that have to be annually re-balanced, withdrawal strategies that involve half a page of instructions and annual recalculations and alternatives to simple annual re-balancing that aim to improve the SWR and portfolio duration. Yet much of this complexity only brings about marginal improvements based on historical data which may never be replicated. Simple strategies whose implementation is pretty “idiot proof” are more likely to endure the 20+ years of a typical retirement and can easily be handed over to a family member or adviser should the retiree no longer have the ability or will to continue with his financial management.

The “Experts” Rarely Agree. Life would be so much easier if given a particular set of retirement circumstances that there would be universal agreement on a plan of action. But that certainly isn`t the case. For instance in academic circles, lifetime annuities are recognised as the only solution to the longevity dilemma being the only product on the market that won`t be outlived by the retiree, yet they are generally unpopular with advisors and their clients. The famous 4% rule is much debated and in 2021 its creator William Bengen argued that 4% was probably too conservative and 4.5% was perfectly safe for the US retiree. But in 2022 Morningstar published a research paper The State of Retirement Income: Safe Withdrawal Rates which proposed that 3.3% was the safe withdrawal rate based upon projections for the stock and bond markets. There are also many published retirement portfolios designed by well-respected financial experts such as Ray Dalio, Bill Bernstein, David Swensen, and Larry Swedroe …. yet when they are compared using tools such as Monte Carlo analysis they often show very contrasting performances.

Very often the differences in expert opinions are not because their analysis is flawed but because they are using different data sets, time periods, and assumptions about acceptable failure rates. These are exactly the same assumptions that the retiree has to make when designing his retirement plan.

Don`t Tinker. Most investors underperform the indices they are investing in because they just won`t leave things alone. They try to time the market or panic sell when the market is falling and buy when it is rising. Do nothing is the best advice for most investors. Retirees have another reason why they should leave their finances on auto-pilot - the risk of poor decision-making due to mental impairment. If at all possible retirees should adopt a strategy that needs minimum maintenance and modification.

Don`t Aim for Perfection. When there is such uncertainty about the key variables of the market, inflation, and longevity then it is pointless trying to achieve the perfect choice of assets, the best portfolio, the optimum Safe Withdrawal Rate, the ideal variable withdrawal strategy, etc. The margin for variation is so great that whilst a strategy that yields a 4.2% Safe Withdrawal Rate may appear to be better than an alternative strategy that yields 4.0% it is highly likely that the actual performance will be way off the theoretical. So don`t become obsessed with marginal differences between options.

Be prepared for changes in personal circumstances. Many pre-retirees dream of the ideal retirement, long holidays, and time to pursue their favourite pastimes in an environment free of the stresses of work, kids, and tight finances. Be prepared for life`s events that tend to upset the best-laid plans: divorce, a new partner (a new family), illness, grown-up kids’ problems, and most tragically death. Think what would happen in the event of divorce. Could your finances survive after asset splitting? Grey Divorce (as it is termed in the USA) is increasing whilst the overall UK divorce rate is falling. The number divorcing over 65 increased by 23% in 2017 for men and 38% for women. It is thought that better health and longer life expectancy are the two main factors responsible.

History may not be the best guide to the future. All retirement financial planning is based upon historical data including the parameters for Monte Carlo Simulation yet we all have seen the warnings that “historical performance is no guide to future performance”. This means that even if the analysis indicates that your plan may have a 99% chance of success there is still a risk. To counter this the retiree must have a significant proportion of his income independent of stock market performance, inflation levels, and longevity.

Money is important but isn`t the key to having an enjoyable and fruitful later life. Providing you have sufficient money to cover your basic needs it has been shown that the greatest contribution to happiness in retirement is your social interaction. A good network of friends and family leads to a happier and longer life.