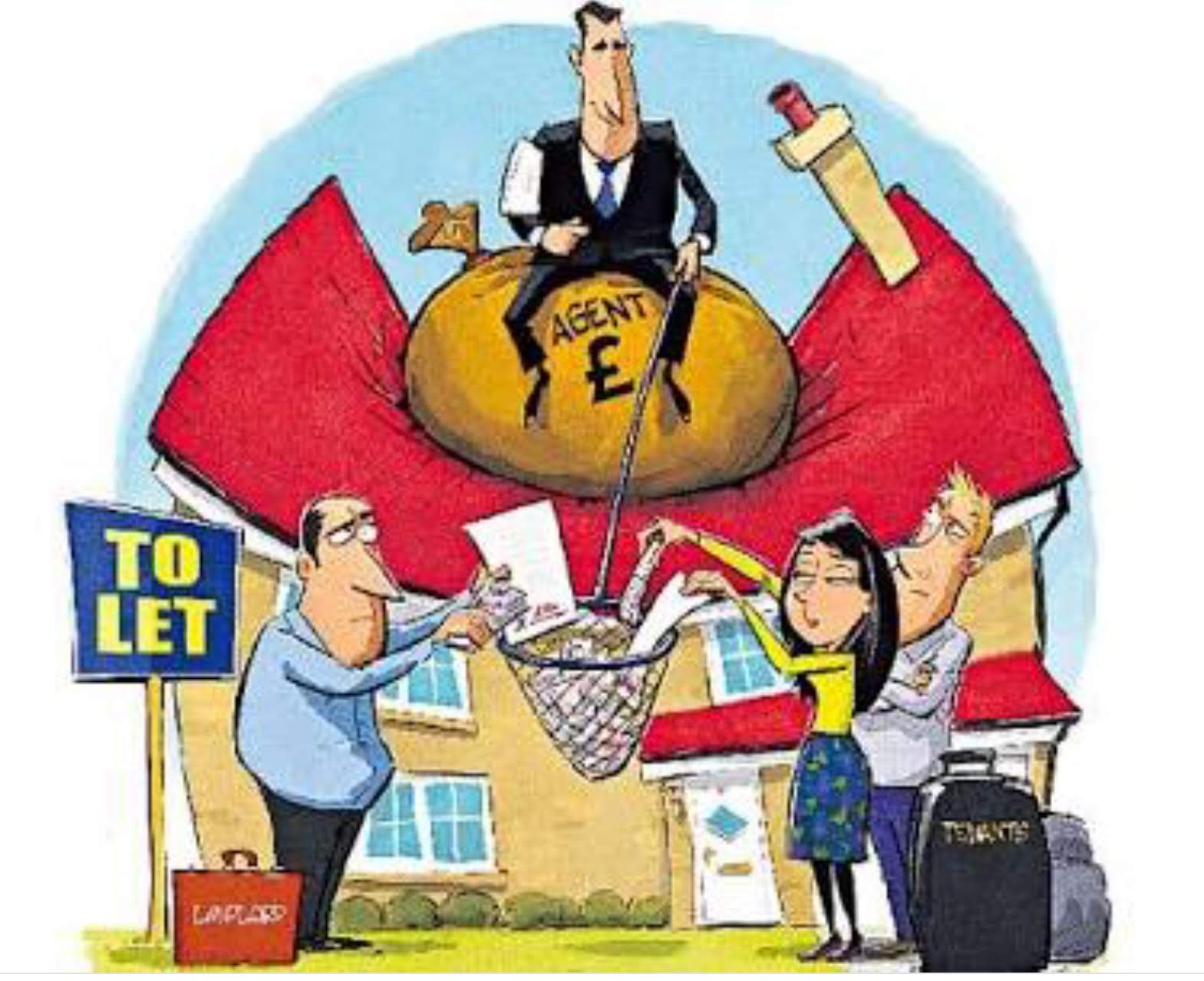

I’ve nothing against Buy to Let, in fact during the last 30 years I’ve owned various properties either as an accidental landlord or for investment. Without doubt I’ve made money through it and accumulated a fair bit of capital. I’ve had some excellent tenants and some disasters but all in all the rental income covered my operating costs and I made a reasonable capital gain.

As any landlord will know renting property isn’t stress free - one can have a year or two with an excellent tenant, rent paid on time and no major maintenance expenses, then suddenly the boiler gives up the ghost, the guttering disappears in a storm, the washing machine dies …. the good tenant leaves and a not-so-good one arrives - the rent starts to arrive a week or so late - every minor problem from a dripping tap to a dead thermostat battery results in a £60 call out charge. But a landlord has to take all of this on the chin knowing that there’s a profit to be made - eventually.

Turning back the clock 30 years, knowing what I now know would I do it again? Without hesitation. Despite the tax changes and denigration of private landlords there are few other investments available to a private individual that allow a high level of pretty much risk free leverage - just so long as one is prepared to ride out the ups and downs of the UK property market. But for retirement income a definite NO. Too much hassle and stress for a low net yield that at times is very sporadic, the ever present risk of being hit by high one off expenses and the drawback of owning a valuable asset but one that is highly illiquid.