I guess ignorance is bliss - I hadn´t realised how complex the issue of drawdown strategy was until I started investigating the subject a few months ago. Without doubt, the accumulation phase is the easy bit - devising the withdrawal strategy is the greatest challenge.

I guess that for most retirees saving for retirement is almost a background activity especially when young when retirement seems a lifetime away and is the least of the preoccupations of youth but membership of a company scheme or the new automatic enrolment scheme will have started many on the road to building a pension pot almost unconsciously. Certainly in my case, one of the greatest contributions to my pension savings was my first 10 years after graduating when I was in a company scheme and this I then transferred into a SIPP and this initial investment grew by a factor of 8 over the years. During the rest of my working life, I contributed as much as I reasonably could but was never over-obsessed by its performance - except perhaps during the last 10 years when retirement started to loom. I am sure that those within the FIRE community aren´t as relaxed as I was!

It may seem strange that only after entering retirement that am I starting to analyze how I am going to live off my pension fund and only now have realised how much more complex an issue this is than the accumulation phase. I guess my prior lack of interest in this was due to two factors. Firstly it was always my intention to enter retirement with a ¨living off dividends¨ strategy. This is to avoid sequence risk - a market crash during the first few years of retirement and also due to my aversion to bonds - I preferred to accept the market ups and downs in return for higher long term growth. Secondly during the last decade or so the dominant topic in the media about retirement was always the choice between purchasing an annuity or drawdown. There was little discussion about drawdown strategy just debate whether a 4% drawdown rate was realistic. Even recent articles in the main stream media about the FIRE movement have trivialised the challenges of drawdown by stating that all you have to do is accumulate saving equal to 25 times your desired income and say goodbye to work for ever - no matter whether you´re 30 years or 70 years old - it ain’t so simple!

What is interesting is that many of the bloggers from the FIRE community who have succeeded in achieving FIRE and have entered the de-accumulation phase are drawing down far less than 4% and I recollect that the statistic for UK drawdown pensioners was about 3.2%. This highlights the essential difference in risk between accumulation and drawdown. In saving for retirement if you

don´t reach your savings target by your hoped-for retirement date you have the options of working a bit longer, taking part-time work or having to be more economical in retirement. In drawdown there is the real fear of outliving your savings due to market poor performance or the good fortune to have excellent health and this fear leads many pensioners to drawdown far less than analysis shows to be possible, resulting in them having less income during the early years of retirement when they are most likely to be healthy and active and most appreciate additional income.

There are three elements to a drawdown strategy and in future blogs, I will explore each one in greater depth:-

- The investment portfolio

- Initial drawdown rate

- Drawdown strategy

It´s quite possible to implement a simple reasonably effective but non-optimum strategy by opting for a 60/40 equity/bond portfolio rebalanced once a year and with an initial drawdown rate of 3 to 3.5% with the income withdrawn increasing annually by the rate of inflation and it is almost 100% certain that the retiree would ever run out of money.

However, this would be non-optimum because it would not maximise the income of the retiree. A Montecarlo simulation of a 60/40 international portfolio shows that 90% of retirees (30 year retirement) could have withdrawn at 4.9% and 50% or more could have withdrawn at over 7%. Or looked at another way 50% of retirees could have had at least 100% more income.

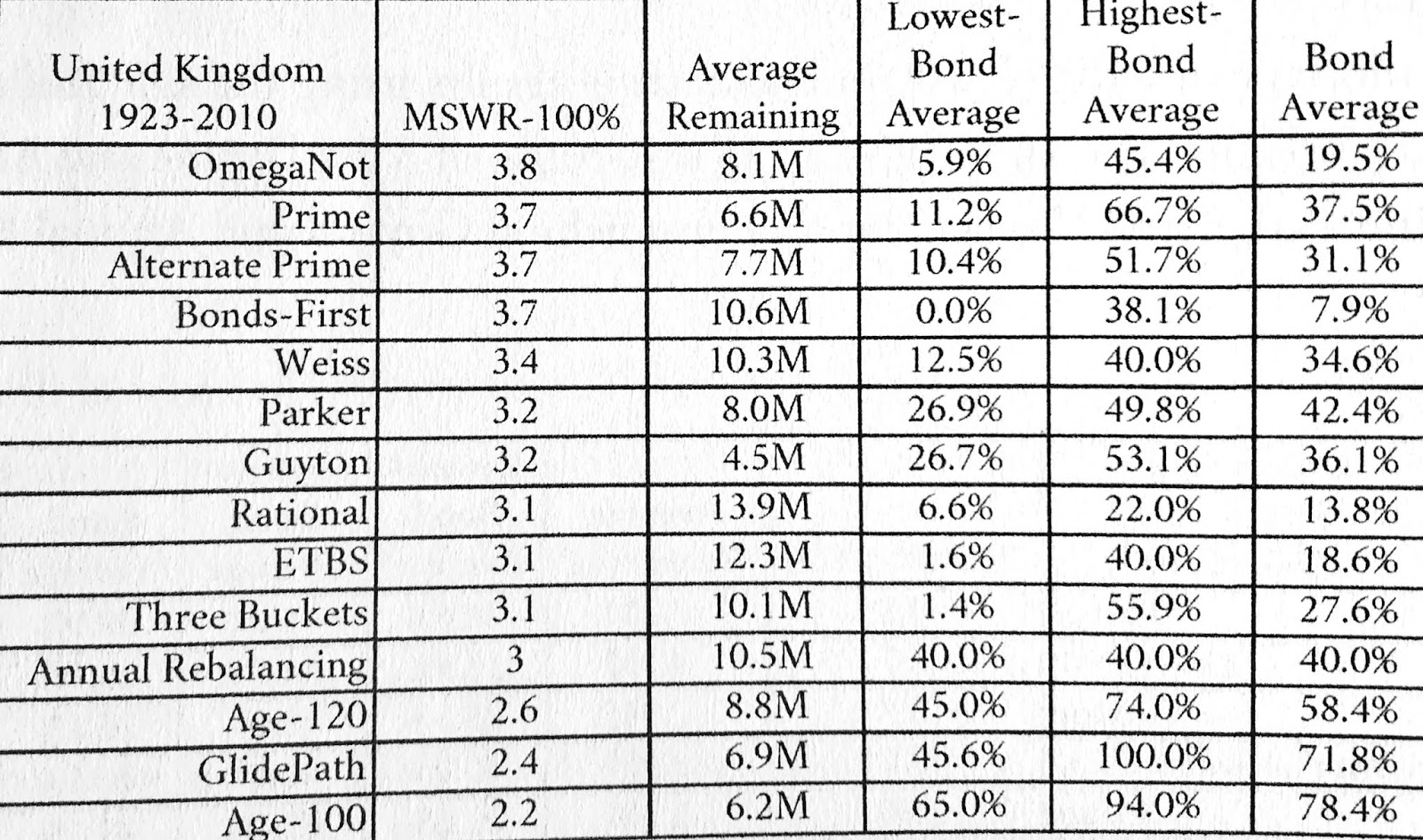

The above assumed a fixed equity/bond ratio (annually rebalanced). There are many alternative withdrawal strategies that vary the equity/bond mix and impact on the maximum safe withdrawal rate (MSR). In his book ¨Living off Your Money¨ Michael McClung compares 14 different withdrawal strategies for the UK market between 1923 and 2010.

|

Comparison of Withdrawal Strategies UK 1923 to 2010 |

The classic 60/40 annually rebalanced portfolio allows a maximum safe withdrawal rate of 3% compared with the optimum “OmegaNot” strategy´s 3.8%.