Maybe Not Ideal For Retirees

I´ve always been quite attracted to the idea of life strategy-type funds such as LifeStrategy from Vanguard and MyMap from BlackRock. In fact, I own both 80/20 and 60/40 funds from Vanguard. The concept of these funds is to have a mix of bonds and equities plus in the case of BlackRock a small dose of alternatives such as property all designed to provide a determined range or risk and volatility in order to meet the needs of investors at various stages of their investment life cycle. So a youngish investor who can tolerate high risk would probably go for a fund predominately invested in shares to provide higher growth but with higher volatility and someone more risk-averse such as a retiree would invest in a fund overweight in bonds. The Vanguard and BlackRock funds provide low costs, diversification, and automatic periodic rebalancing.

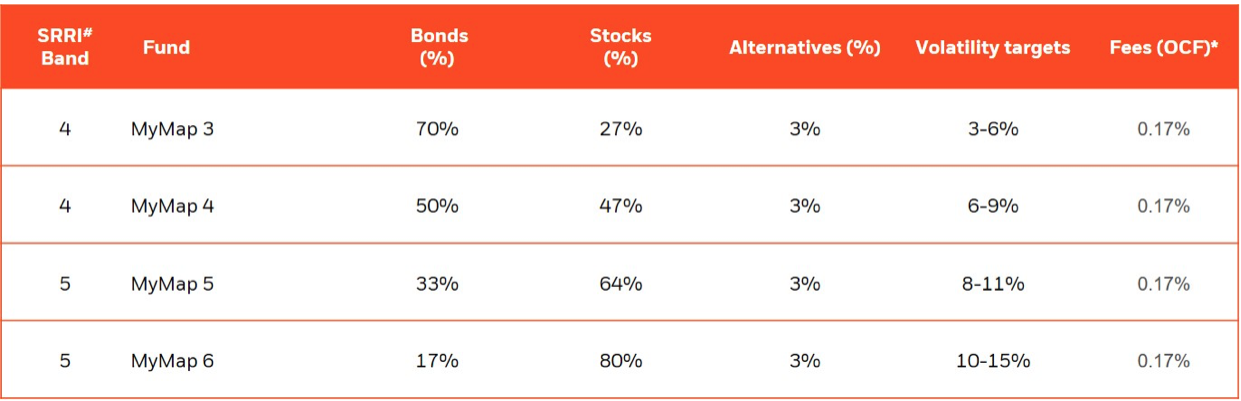

BlackRock has 4 funds with different equity/bond allocations which provide varying levels of risk/volatility/return. Unlike Vanguard BlackRock can vary the equity/bond ratio in accordance with market conditions.

|

| BlackRock MyMap Funds

|

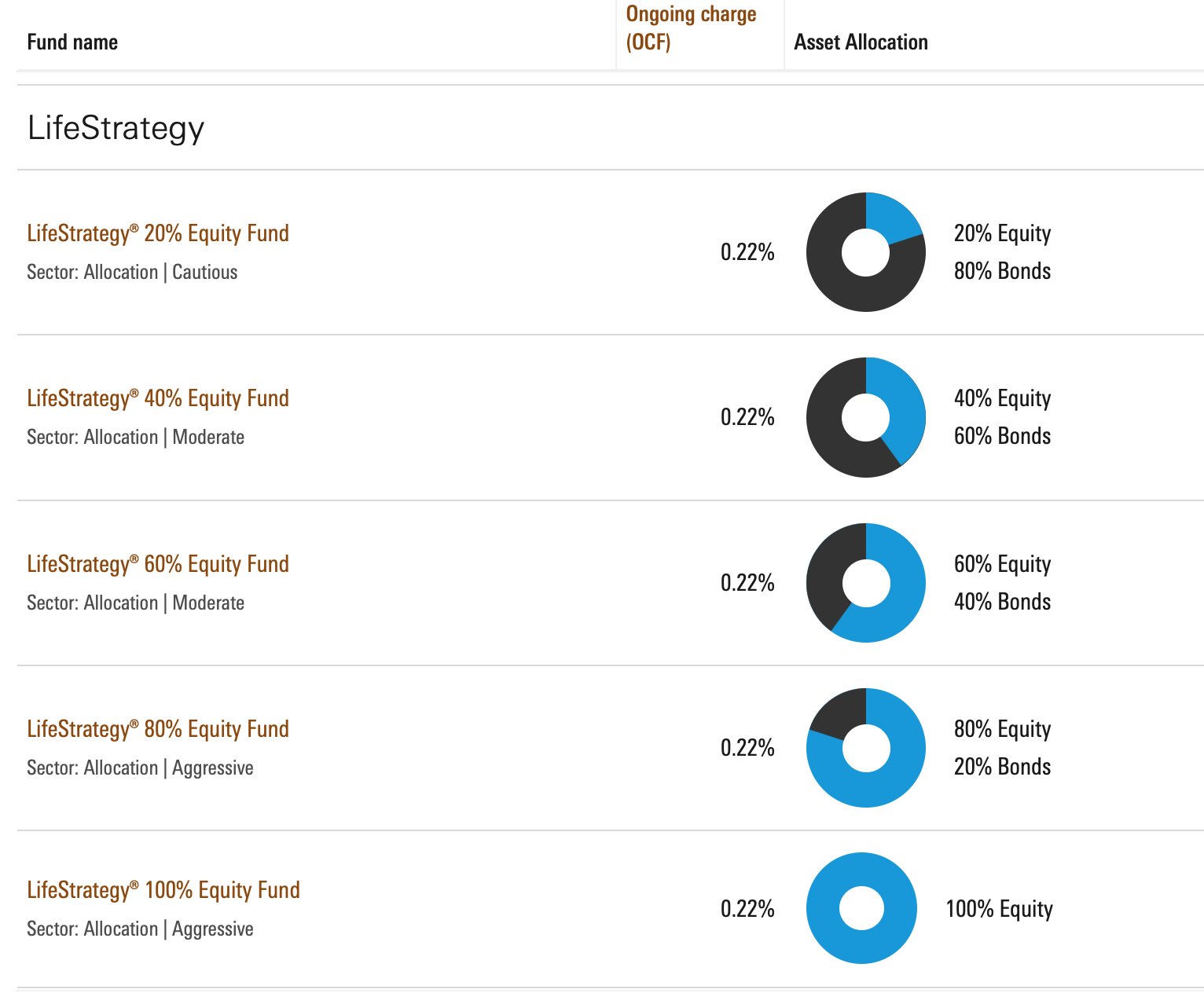

Vanguard offers 5 funds with equity/bond ratios varying from 100% equity to 20% equity/80% bond and unlike BlackRock aims to maintain the ratios constant through frequent re-balancing.

|

| Vanguard LifeStrategy Funds |

Vanguard in the USA published an interesting analysis of the historical performance of equity/bond portfolios which although based on USA markets does illustrate the trade-off between volatility and portfolio growth. Here are examples of two portfolios:-

|

| 20% Equity/80% Bond Portfolio |

|

| 80 equity/20% Bond Portfolio |

I have only held my LifeStrategy fund for a year or so and certainly have no complaints - performance has exceeded my expectations - probably as a consequence of its overseas holdings benefiting from the sterling devaluation during the Brexit turbulence - but then that is the idea of having a diversified portfolio. So why am I now getting cold feet? Retirement! My principal sources of investment income are from dividend portfolios and from drawdown portfolios and in the case of the latter, it was my intention to use Vanguard LifeStrategy funds.

There are three crucial factors in drawdown which the retiree must determine: the portfolio, the drawdown strategy and the initial drawdown income. The characteristics of Vanguard´s LifeStrategy funds are directly relevant to my portfolio objectives and drawdown strategy.

Portfolio Bond Characteristics

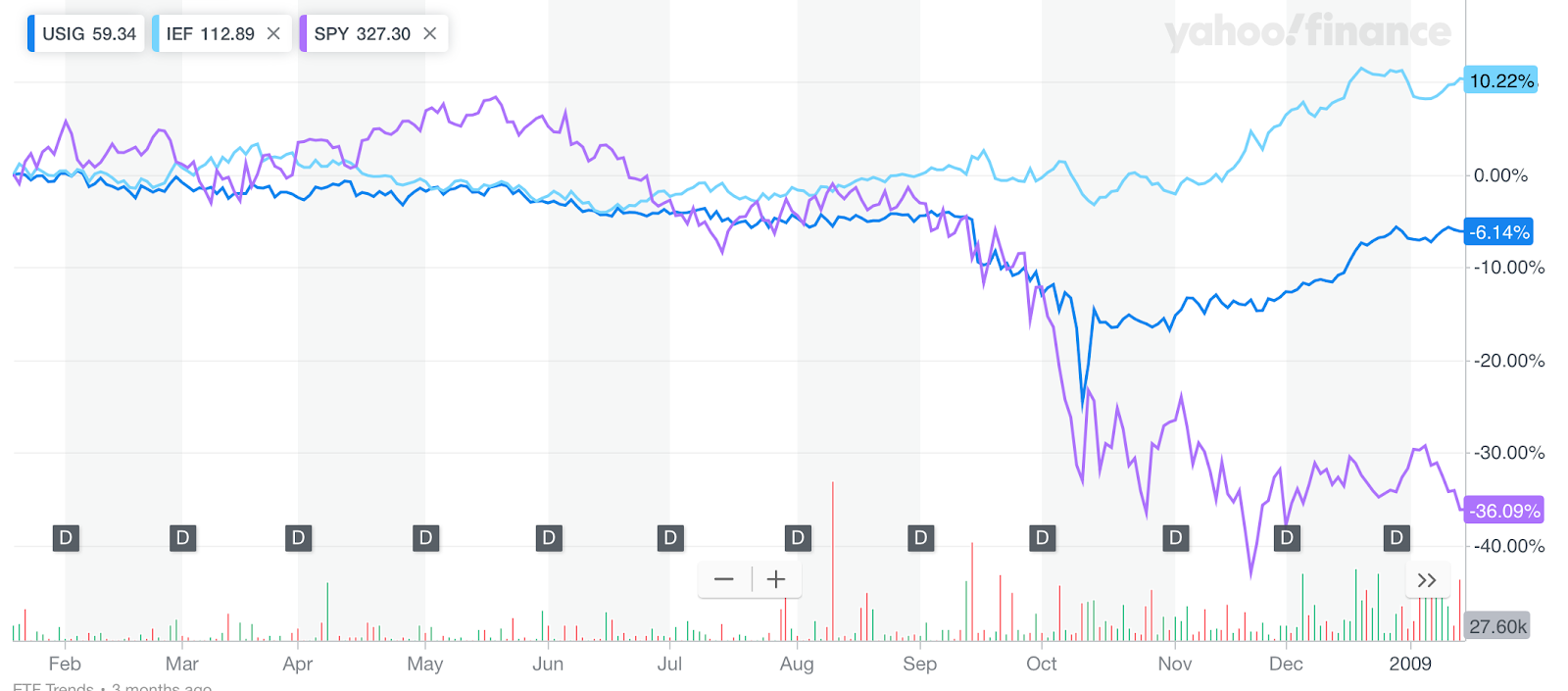

I don´t intend to discuss the portfolio design here but any retirement portfolio is likely to include bonds as insurance to reduce volatility - but not any old bonds - they must be government bonds because only these will provide a safe have during market downturns as they are negatively correlated with share prices, unlike corporate bonds which although they will show greater resilience than shares they will still decline.

|

| Crash of 2008 - S&P 500, Intermediate Treasuries, High-Quality Corporate Bonds |

Have you decided which alternatives to the available Life Strategy Funds you may use?

Good question?! I’ve been doing a lot of analysis in order to design a portfolio that will maximise the safe withdrawal rate - there are some great tools available but most geared to ETFs and funds only easily accessible to US investors - had I been in the USA I would have gone for 50% equity, 50% intermediate treasuries with the equities split 30/20/10 s&p 500/international /global small cap value using Vanguard or Ishares ETFs. I’m still working on the best options as a UK investor and will post my conclusions some time over the next few weeks.

Thanks for the response.

I look forward to reading your conclusions for the UK investor.