I have just read a Trustnet article titled “Three reasons why Vanguard’s LifeStrategy range is outperforming in 2020″ and thought …really?!. Of course any fund holding bonds and in particular gilts or treasuries should have outperformed the 100% equity indices or funds.

I was fairly negative from the viewpoint of a retiree about LifeStrategy in my post “Falling Out of love with LifeStrategy Funds“. In particular I was unhappy with the presence of corporate bonds. The most important role bonds have in a portfolio is “de-risking” - reducing the volatility of the portfolio and in the event of a market downturn moving in the opposite direction to equities. Only government bonds can do this and the longer the duration the bond the greater the effect.

The other negative for me was the very concept of an auto balancing equity/bond portfolio. This in many respects is a great convenience and plus for many investors but when in drawdown there are withdrawal strategies that favour selling bond holdings in market downturns in order to avoid selling equities at low valuations and in order to preserve the higher growth equities holdings. A LifeStrategy fund doesn´t give this flexibility.

An issue that I didn´t address in my previous post was that of currency hedging. The pros and cons of currency hedged investments are complex and is a topic that I´ll be examining in a future post. The majority of overseas index funds such as those tracking the US S&P 500 are currency hedged so if the index moves by 10% so will the fund with a small variation due to hedging cost and errors. For a UK investor this reduces volatility as movements of sterling against the US dollar don´t have an impact. The disadvantage is that an investor in international hedged funds doesn´t benefit from sterling weakness which occurred during the Covid-19 market crash and the post the Brexit referendum. An investor in an unhedged MSCI World fund would have seen a gain over 5 years up to the end of 2019 of about 50% whereas an investor in the unhedged fund would have gained 75%. The majority of LifeStrategy overseas bond and equity holdings are sterling hedged.

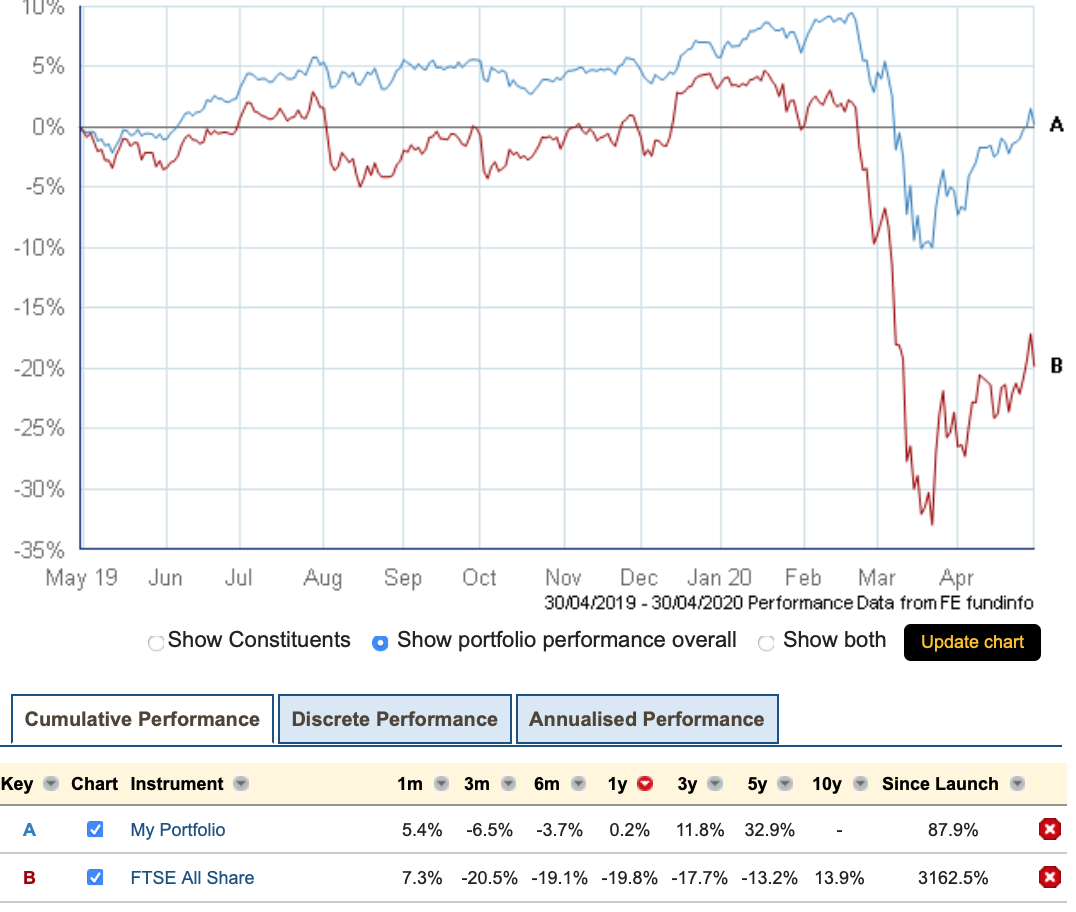

LifeStrategy 60/40 Performance

|

LifeStrategy 60/40 v FTSE All Share |

Any LifeStrategy 60/40 investor would have been relieved by its performance during the Covid crash. Whilst the FTSE All share fell by nearly 40% from its 12 month peak LifeStrategy fell 18% from its peak and over 12 months it was up 0.2% compared with a near 20% fall in the FTSE. Over 5 years LifeStrategy was up 32.9% compared to a decline of 13.2% in the FTSE (all figures are total return).

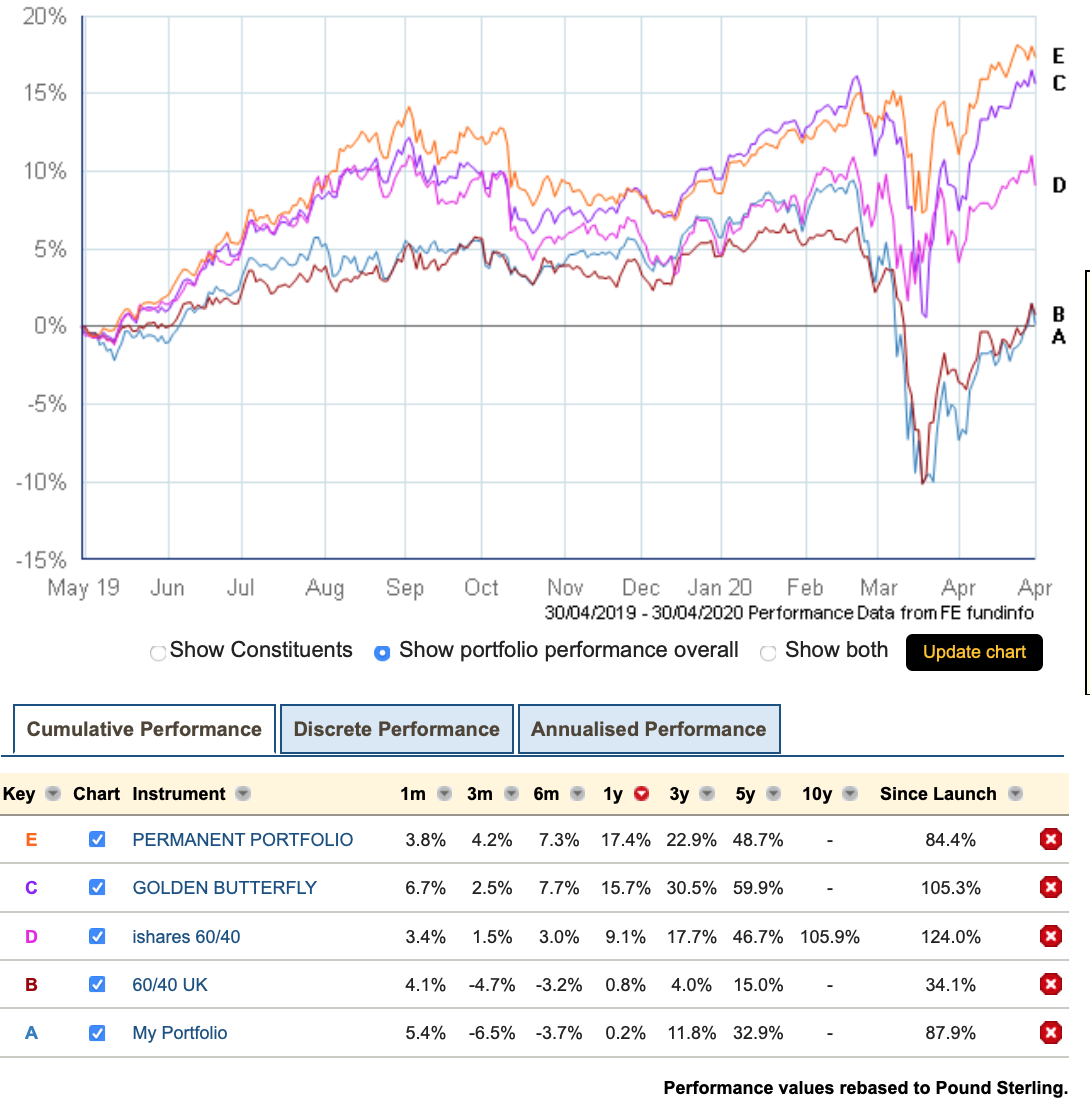

But how does the LifeStrategy 60/40 perform against other portfolios. In general the answer is not so well:-

In the above graph and table “My Portfolio” is the LifeStrategy 60/40. It is compared with 4 other mixed asset portfolios:-

Permanent Portfolio:this is a Harry Browne style portfolio with equal parts gold, cash, MSCI world equity and long gilts. I have operated this since September 2019 (see post).

Golden Butterfly: this is essentially a permanent Portfolio with 40% equity divided between total market and ideally small cap value (I substituted small cap ITs), 20% gold, 20% cash, 20% long term gilt (see Golden Butterfly post).

Ishares 60/40: 60% MSCI World equity and 40% SPDR long gilt.

60/40 UK: 60% FTSE All Share, 40% Ishares all gilt ETF

Only the 60/40 UK portfolio underperformed the LifeStrategy fund. It was up 15% over 5 years compared to the FTSE All Share Index but it illustrates the importance of having international diversification in a portfolio. All the other portfolios outperformed LifeStrategy over 1, 3 and 5 years and in the case of the Permanent Portfolio and Golden Butterfly by a large margin. They also exhibited lower volatility all gaining a little over the last 3 months compared to a 6.5% decline in LifeStrategy.

Conclusions

To answer the question posed in the title “Have They Really Out-Performed in 2020?” the answer has to be yes and no. As with most things in investment finance there is rarely a definitive answer as it depends upon your perspective. There are certainly other portfolios which over the last 5 years offered lower volatility and higher growth but there are also many that had greater volatility and lower growth. If I were at a different stage of my investment life I would certainly consider a LifeStrategy fund as they provide low cost, diversified funds where you can choose your level of risk dependent upon your personal circumstances. And later in life when I will need simple to maintain investments they will probably be at the top of my list of options.