Long term government bonds can play a vital role in a retirement portfolio providing protection both during periods of deflation and market crisis. However, whether now is the time to buy is another story! With long term interest rates at near zero levels it´s difficult to find any commentator forecasting a rosy future for long term gilts or US treasury bonds. But ever since the 2008 financial crisis and the collapse in interest rates and rise in bond price experts have been forecasting the crash of the bond market and it hasn´t happened - yet.

Back in 2016 Paul Singer, the billionaire founder of investment firm Elliott Management warned that “The term ‘safe haven’ applied to G-7 bonds is just wrong,These are not safe havens. In fact, there’s a tremendous amount of risk in owning 10- and 20- and 30-year bonds at these rates.”

But - you would have been pretty happy had you ignored his advice as 20 year US treasuries rose from $135 to $168 from September 2016 when Singer made his comments to May this year. Long term government bonds did what they normally do when the stock market crashes -jumped in price (all be it - like gold - after an initial fall as some investors went for cash).

|

ISHARES 20 YEAR US TREASURY ETF |

Despite this unpredicted resilience pessimism for the future of bonds persists. Most recently, highly respected Wharton professor Jeremy Siegel explained on CNBC why the bond market’s 40-year bull run is doomed. The reasons are similar to those posited after 2008 in that the unprecedented government Covid-19 borrowings will fuel inflation, interest rates will rise and bond prices will fall.

Siegel is not alone in his outlook but if you check the internet you´ll find forecasts from some of the most well know financial experts during the last 20 years predicting the “end of the bond bubble”. However, this time surely surely they´ll be right as bond yields can´t get much lower - or can they?!

|

10 YEAR US TREASURY YIELD |

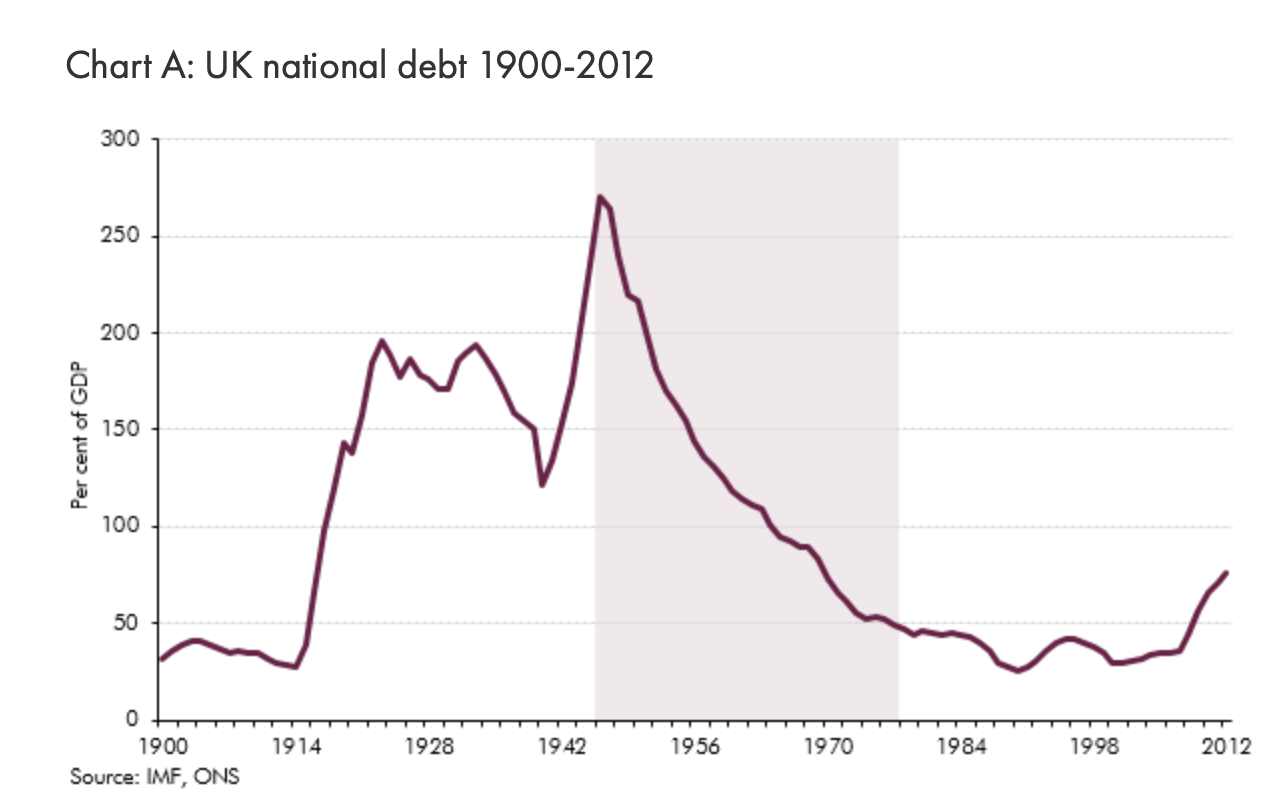

In the UK we are being told that Covid-19 borrowings will increase by at least £330m and probably much more and take our total borrowings to levels not seen since the end of the 2nd World War when they reached over 270% of GDP.

|

UK Post 2nd World War National Debt (OBR) |

The interesting fact is that the UK´s GDP in 1946 was around £10bn and debt £27bn. By 2019 the UK´s GDP had increased to £2,825bn so due to the miracle of inflation and GDP growth that massive post war debt represents less than 1% of today´s GDP. One has to suspect that the governments and central banks won´t be in much of a hurry to curb inflation over the next 50 years.

High inflation and perhaps significantly higher interest rates certainly don´t favour holders of long dated bonds. However, as investors we should be happier with some inflation rather than 30´s style deflation and holders of well designed portfolios should have constituents that protect against all economic environments - the Permanent Portfolio and Golden Butterfly Portfolios are both examples of portfolios that have asset classes (including long term bonds) that are uncorrelated and provide protection and growth prospects in all market conditions.

If the Outlook is so Gloomy Why Hold Long Term Bonds?

Firstly lets look at why we should hold any bonds at all in a portfolio. 30 years or so ago the personal finance pages of the press promoted bonds as providing a regular income with safety of capital. I don´t think you´ll find any such recommendations today after a decade or of near zero interest rates. This traditional income generator role of bonds has largely been forgotten and focus is now on bonds in their function of de-risking portfolios enabling the investor to find a balance between growth and volatility.

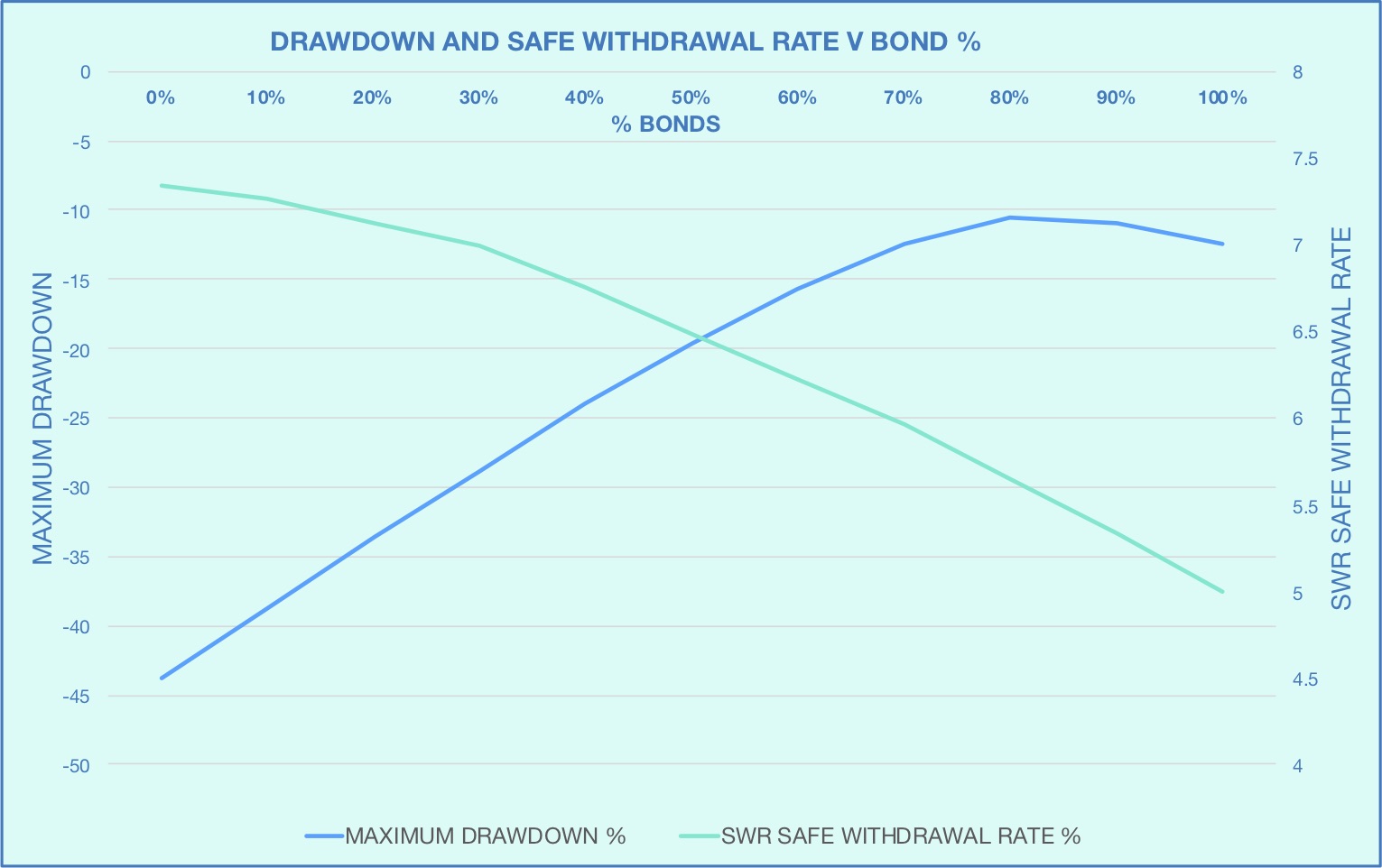

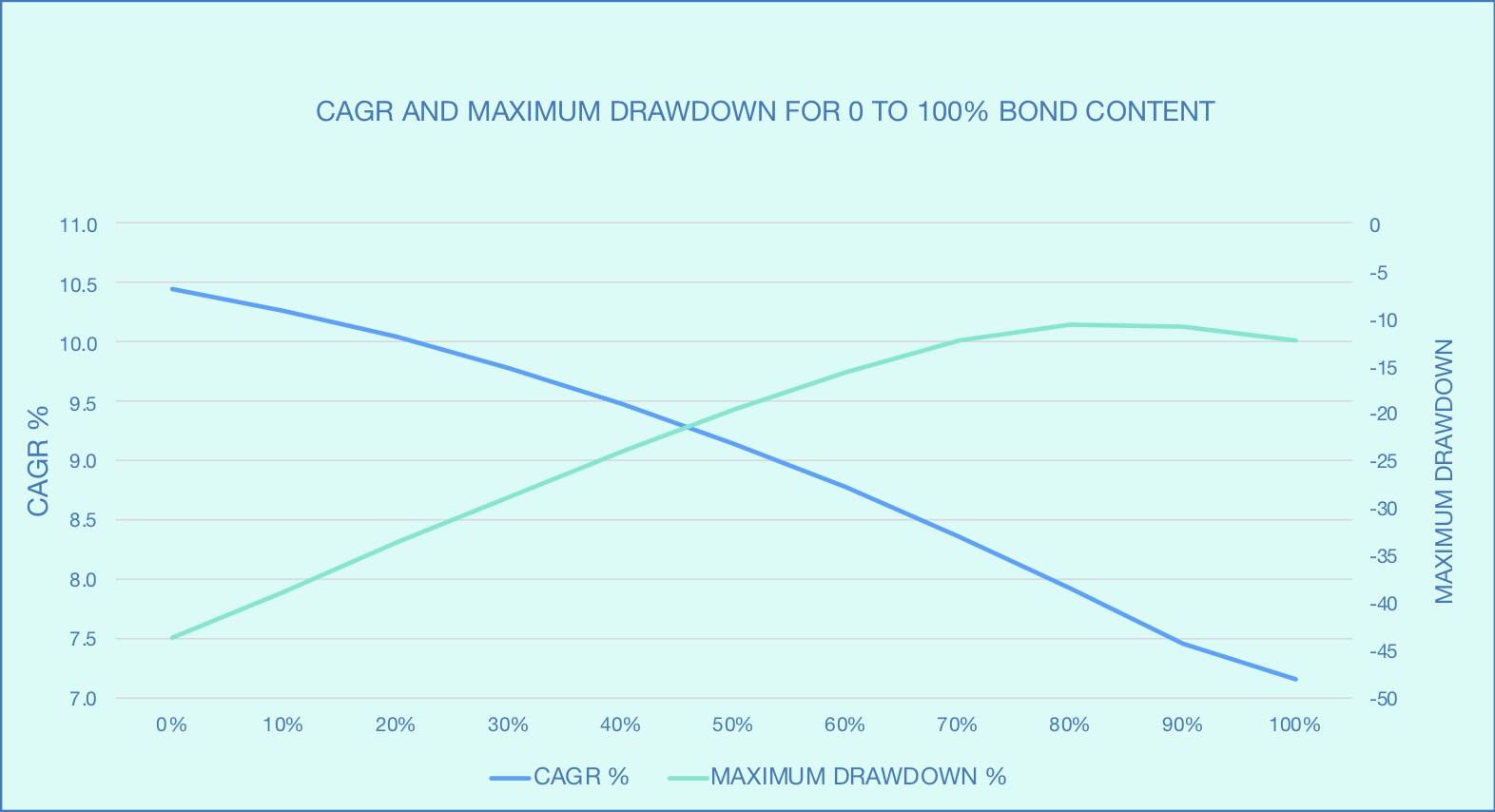

In the first graph below the maximum drawdown and Safe Withdrawal Rate (SWR) are shown for equity/bond portfolios comprising of the total US Stock Market and Treasury Intermediate Bonds ranging from 100% equity to 100% bond. In the second graph the Compound Annual Growth Rate (CAGR) is shown. The data is produced using Monte Carlo Simulation with market statistics from from 1972 to 2020. (Apologies for focussing on US assets but data and analysis tools are more readily available).

|

US TOTAL MARKET/INTERMEDIATE TREASURY BONDS PORTFOLIO

The relationship between bond % and risk/return is very clear. A 100% equity portfolio has a 10.44% CAGR, permits a 7.3% Safe Withdrawal Rate but has a 43.7% drawdown risk. A 100% bond portfolio only provides a 7.15% return and a 5% SWR but the investor suffers a modest maximum worst case situation fall in value of 14.45%. Bonds allow the investor to optimise his portfolio in accordance with his appetite for risk and need for growth.

|

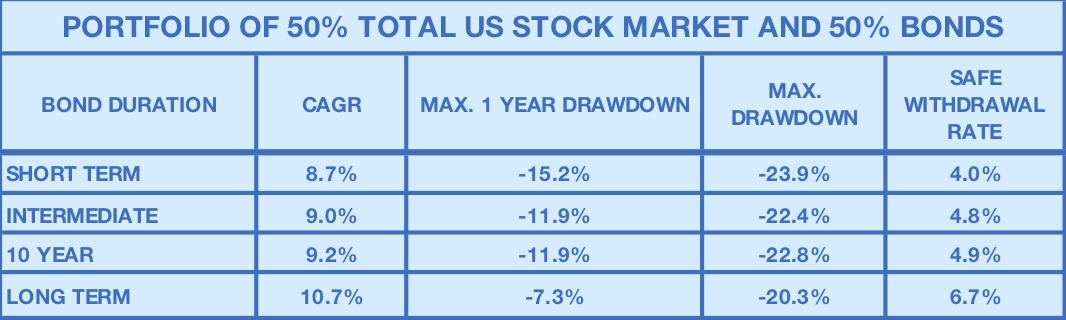

So Which Bonds are Best?

The effect of bond duration on portfolio performance can be seen from the table below which looks at historic 50/50 equity bond portfolios (US total market/treasuries) with bonds of varying duration over the periods from 1977 to 2010. The results are clear - as the duration of the bonds increase so does the growth rate (CAGR) and Safe Withdrawal Rate whilst the maximum drawdown decreases. Some caution is required looking at these figures as for much of the period covered by the data bond yields were decreasing so the growth rates for long term bonds were high at over 8% CAGR - its difficult to believe that this can be repeated over the next 30 years however long bonds will still be the most effective instrument for reducing portfolio volatility.

To Invest or Not To Invest - and How?

Any holder of long term bonds at the moment is unlikely to be regretting their purchase in view of their excellent performance in response to the Covid-19 market crash. How much is a sensible holding? I would be happy with between 10% and 20% of my portfolio being in long dated bonds.

My own holding of long term gilts purchased in September 2019 is up over 10% and has helped (together with gold and cash) to increase my portfolio value by over 5% since September despite the crash in equity values. Do I think they should continue in my portfolio? Yes. Will I increase my holding in the near future? No. If I were to rebalance the portfolio now I would be selling gold and long term bonds and purchasing equities. In fact I plan be investing more cash in the portfolio over the next month so will leave the gold and bonds alone and top up my equity holdings.

The advantage of having a balanced existing portfolio is that one can make small adjustments through rebalancing. For someone starting from scratch or wanting to make a major shift in asset allocation life is more complicated. There will always be assets in a portfolio that seem destined to fall and others to rise. Gold and bonds have had a good run and some equities a hard time. But predicting the future direction of markets is a game that very few master and anyway the theory is that asset prices reflect expert views so there are no bargains or over priced assets around - supposedly!

Long bonds should be part of every retirement portfolio but for someone who wants to buy into long term bonds for the first time timing that investment is not an easy decision given current valuations. I have been in similar situations many times and the only approach that has given me peace of mind is to phase my purchases over a reasonable time scale say 12-24 months. This is against most expert advice that shows when lump sum investing the probability is that you will achieve higher growth making a single purchase rather than spreading purchases over a period of time. This advice is based upon the fact that markets spend more time rising than falling so the probability is that you will invest at a time when you can benefit from rising prices. Vanguard´s guide to lump sum investing states that historically a lump sum investment will outperform phased investment 70% of the time. I don´t like the odds! 30% of the time if I invest all at once I´ll see my investment fall in the short term. I will have far more restful nights pound cost averaging than gambling on the 70% chance of a 2% short term improvement in return. But that´s me - too old to take risks!

How to Invest

UK investors do not have many options available if they want to buy into long dated gilts. Of course there is always the option of purchasing individual gilts direct but this involves administration in creating and maintaining a gilts portfolio. The alternative in an ETF or fund. There is limited choice and the most accessible are SPDR® Bloomberg Barclays 15+ Year Gilt UCITS ETF (GLTL.LN) and Vanguard U.K. Long Duration Gilt Index Fund. Both track the same index and have comparable costs and performance. Probably the main deciding factor will be costs. There are usually higher trading costs associated with ETFs but often such as the case with AJ Bell potentially lower holding costs compared to funds. The disadvantage of when trading funds is you do not know the purchase or sale prices at the time of executing a transaction. I have found this frustrating having sold some funds at various times over the last few months.

The other option for UK investors is an All Gilts ETF or fund to have exposure to all gilt durations.

For an investor who wants the simplicity of a two fund equity/bond portfolio this is an attractive option and the majority of ETF and fund index tracking providers offer low cost products. There are however variations in composition of the trackers depending upon the index they track. Vanguard offers an ETF (VGOV) and fund both of which track the Bloomberg Barclays Sterling Gilt Float Adjusted Index whereas the popular Ishares ETF (IGLT) tracks the FTSE Actuaries UK Conventional Gilts All Stocks Index. Vanguard has 58% allocated to gilts 15 years or longer and Ishares 47% with the average duration of Vanguard is around 2 years longer than Ishares. 5 year performance of the two is nearly identical but over the last 12 months Vanguard gained 13.6% compared to 11.96% from Ishares. Periods of declining interest rates will tend to slightly favour the longer duration Vanguard products but when rates rise the opposite will be true.

US Treasuries

CONCLUSION

Just as I am concluding this post I recollect a comment in today´s Times. In an article entitled “Gilt yields fall as hope of a quick recovery fades fast” there was the comment from Analysts at Capital Economics “As a protracted economic recovery from the coronavirus crisis will force the Bank to keep interest rates close to zero and further expand its quantitative easing programme, gilt yields will probably stay very low for many years.” The reality is that no analyst can predict the future of interest rates. The only option for private investors is to avoid market timing by phasing investments over time and by having a well diversified portfolio - in which it is my belief that long dated government bonds should play a part.