How are you feeling about your retirement portfolio? Full of remorse for riding the 10 year bull market or relieved to have invested in a diversified portfolio full of high quality government bonds?

I am suffering from both relief and remorse. Relief because back in September I invested part of my portfolio in a Harry Browne style Permanent Portfolio (up 3%+ over 3 months) and remorse for not investing more and remorse for not selling more individual shares in my SIPP to invest in Income Investment Trusts.

If you are a UK investor and had a diversified portfolio with uncorrelated assets such as government government bonds, gold and a strong international weighting you would have survived the market crash relatively unscathed and outperformed significantly the FTSE All Share both short term and over 5 years. Have a look at how some typical portfolios performed:-

|

Comparison of Retirement Portfolio Performance

|

|||||

|

1 month

|

3 months

|

1 year

|

3 year

|

5 year

|

|

|

The Permanent Portfolio

|

-0.3%

|

3.7%

|

12.7%

|

16.8%

|

37.3%

|

|

The Golden Butterfly

|

-3.7%

|

-1.8%

|

9.6%

|

19.6%

|

43.0%

|

|

UK 60/40

|

-7.3%

|

-8.4%

|

-3.8%

|

-0.9%

|

8.2%

|

|

Global 60/40

|

-2.1%

|

0.7%

|

8.8%

|

10.9%

|

35.4%

|

|

Vanguard LifeStrategy 60/40

|

-10.4%

|

-13.1%

|

-5.7%

|

3.1%

|

22.4%

|

|

FTSE All Share

|

-21.1%

|

-30.2%

|

-27.1%

|

-25.5%

|

-20.0%

|

The Permanent Portfolio, The Golden Butterfly and the Vanguard LifeStrategy I´ve already discussed in some depth in previous posts but I´ll take a look at all the portfolios in the above table later on. But first a quick look at two of the traditional safe havens - gold and government bonds which provide portfolios with assets uncorrelated with the stock market - stocks go down and gold and government bonds go up - well that´s the accepted wisdom:-

GOLD

Gold has always been considered as a safe have investment but is often highly volatile and sometimes surprises - as has happened during our most recent market crash. Gold certainly surprised some surprised with wild swings in price but finally up 2.6% in US$ over the last 60 days - certainly better than the equity markets but a greater “flight to safety” was anticipated - in fact it was cash that was really seen as being king. The UK investor fared a little better as gold did provide some protection

against the fall in the pound rising by 6.7% in sterling terms.

|

| GOLD PRICE IN US DOLLARS |

|

| GOLD PRICE IN £ |

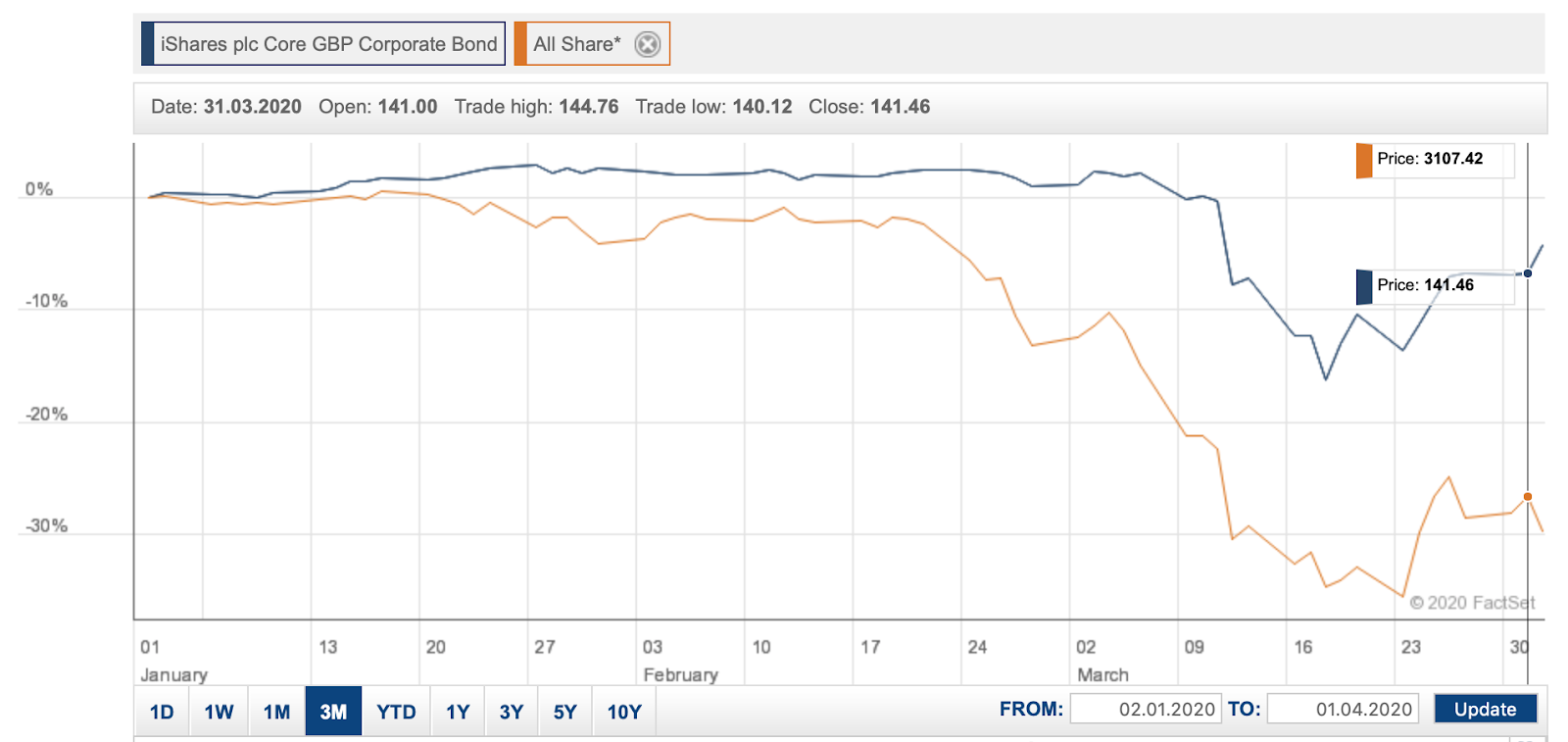

BONDS

Almost 10 years ago I posted about bonds as a safe haven emphasising that only government bonds provide safety during market crashes. The last few months are no exception. Corporate bonds are correlated with stocks and the Ishares UK corporate bond ETF (ISFF) duly tracked the FTSE All Share - all be it not falling so dramatically.

|

Ishares UK Corporate Bond ETF v FTSE All Share |

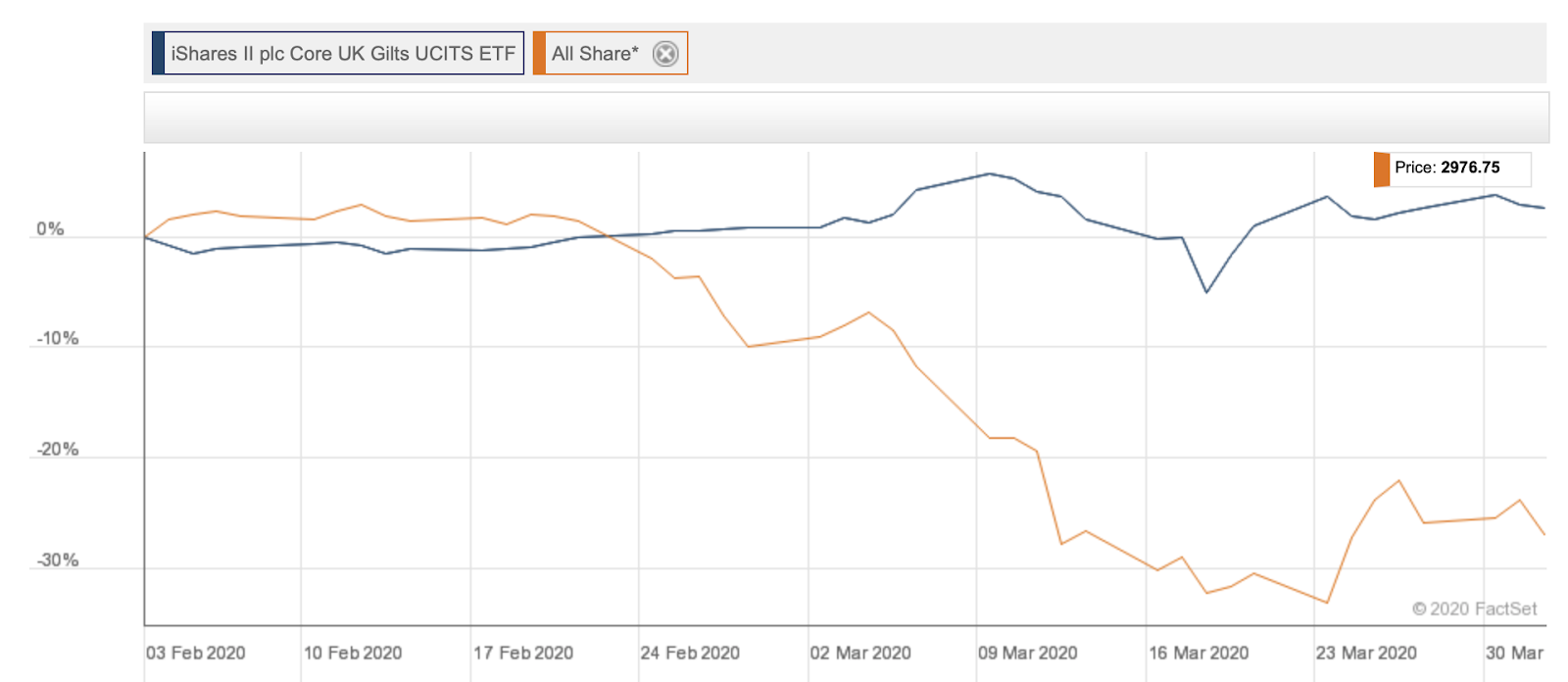

The Ishares UK All Gilt ETF (IGLT) provided better protection but probably not the level than would normally be expected - again cash was king as many traders had to liquidate gilt holdings to meet liabilities.

|

Ishares UK All Gilt ETF v FTSE All Share |

PORTFOLIOS EXAMINED

- Permanent Portfolio

- Golden Butterfly

- UK Based 60/40

- Global 60/40

- Vanguard LifeStrategy 60/40

Permanent Portfolio

I have operated this portfolio since September 2019 with a £50k investment in an account with Iweb.

|

PERMANENT PORTFOLIO (VALUATION 1/APR/2020

|

|||||

|

Company

|

Holding

|

Book Cost

|

Valuation

|

+/-

|

+/-

|

|

ISHARES III PLC CORE MSCI WORLD UCITS ETF

|

264

|

£12433.81

|

£10,274.88

|

(£2,158.93)

|

-14.99%

|

|

ISHARES III PLC UK GILTS 05YR UCITS ETF GB

|

93

|

£12463.42

|

£12,519.66

|

£56.24

|

0.45%

|

|

ISHARES PHYSICAL M ISHS PHYS GOLD ETC USDGBP

|

529

|

£12650.55

|

£13,248.81

|

£598.26

|

4.73%

|

|

VANGUARD INV UK LT UK LONG DUR GILT IDX A GBP

|

54.2151

|

£12419.99

|

£13,000.40

|

£580.41

|

4.67%

|

|

£49967.77

|

£49,043.75

|

(£924.02)

|

-1.85%

|

||

|

PERMANENT PORTFOLIO 5 YEAR PERFORMANCE v FTSE ALL SHARE |

The Golden Butterfly

This came out as the clear winner in my post on retirement portfolio design and I am taking advantage of the market downturn to convert my Permanent Portfolio to the Golden Butterfly by adding 2 UK and 2 Global Small Cap Investment Trusts to my Permanent Portfolio to metamorphosise it into a Golden Butterfly:-

|

GOLDEN BUTTERFLY PORTFOLIO

|

||

|

ASSET

|

%

|

|

|

CASH

|

20%

|

Ishares Gilts 0-5yr

|

|

TOTAL STOCK MARKET

|

20%

|

iShares Core MSCI World ETF

|

|

SMALL CAP UK

|

10%

|

BlackRock Throgmorton IT

Standard Life UK Smaller Companies

|

|

SMALL CAP GLOBAL

|

10%

|

Edinburgh Worldwide IT

Smithson IT

|

|

LONG TERM GILTS

|

20%

|

Vanguard Long Duration UK Gilt Fund

|

|

GOLD

|

20%

|

iShares Physical Gold ETF

|

|

5 Year Performance of Golden Butterfly v FTSE All Share |

Over the last 3 months the Golden Butterfly was down 1.8% compare to a decline of 30.2% in the FTSE All Share and over 5 years up 43% compared with a 20% fall in the FTSE All Share.

60/40 Portfolios

The 60/40 stock/bond portfolio is a traditional home for retirement savings although due to near zero bond yields it has been declared dead by many commentators who have proposed other asset classes as bond alternatives. However, in my analysis of retirement portfolios it performed surprisingly well compared to several of the often promoted alternatives.

I have looked at three variants of the 60/40:-

- Global: MSCI World ETF (60%) SPDR US Treasury 7-10 Year (40%)

- UK:FTSE All Share ETF (60%) Ishares UK All Gilts (40%)

- Vanguard LifeStrategy 60/40

|

Performance of 60/40 Stock/Bond Portfolios

|

|||||

|

1 month

|

3 months

|

1 year

|

3 year

|

5 year

|

|

|

UK

|

-7.3%

|

-8.4%

|

-3.8%

|

-0.9%

|

8.2%

|

|

Global

|

-2.1%

|

0.7%

|

8.8%

|

10.9%

|

35.4%

|

|

Vanguard LifeStrategy 60/40

|

-10.4%

|

-13.1%

|

-5.7%

|

3.1%

|

22.4%

|

|

FTSE All Share

|

-21.1%

|

-30.2%

|

-27.1%

|

-25.5%

|

-20.0%

|

All three portfolios beat the FTSE All Share with the best performer being the Global portfolio followed by Vanguard and lagging by a large margin is the UK 60/40 portfolio. The weak performance of both the UK stock market and the devaluation of sterling due to Brexit and then corona virus severely handicapped portfolios biased towards the UK and sterling. Vanguard LifeStrategy has UK stock and bond holdings which reduced its performance compre to the International portfolio.

So What Can We Learn?

Firstly lets remember that this crisis is far from over and I suspect it will be 12-24 months before we can really draw any firm conclusions about the wisdom or otherwise of our investment decisions. UK investors need to bear in mind that sterling has suffered both through the Brexit vote and now with the Covid-19 market crash. The FTSE All share has also underperformed and the US S&P 500 out performed. This has greatly favoured investors in International equities who have benefited from sterling devaluation and the US market´s strong performance. Hence the Global 60/40 portfolio´s strong performance. Any portfolio containing gold, such as The Permanent Portfolio and the Golden Butterfly will also have provided protection against sterling devaluation and has helped these portfolios to out perform.

One of the biggest lessons I have learnt in recent time is how sterling volatility can have a dramatic influence on our portfolios. Most of us will remember every fall in sterling was accompanied by a rise in the FTSE100 and an increase in the value of our overseas investments - and every fall in sterling made our overseas holidays more expensive and reduced the income of ex-pats. All this of course is reversed if sterling strengthens.

None of us can forecast the future and the only recourse open to us is portfolio diversification to reduce our dependency on any one currency or asset class. Many “experts” however don´t give enough consideration to choosing uncorrelated assets - a basket of 2000 global shares provides diversification by geography, sector and capitalisation but they are not uncorrelated - when the crash comes they will all fall. Corporate bonds are correlated with the stock market. Government bonds are uncorrelated with stock market. Gold in uncorrelated with the stock marker. Property is correlated with the stock market. So we need to have portfolios with a bunch of uncorrelated assets which is why the Permanent Portfolio and the Golden Butterfly have been shown to perform well in all market conditions.